-

Central bank meetings continue in earnest with BoJ, Fed and BoE

-

Fed and BoE to likely stand pat, but BoJ might tweak policy again

-

NFP report and Eurozone flash GDP and CPI data also in focus

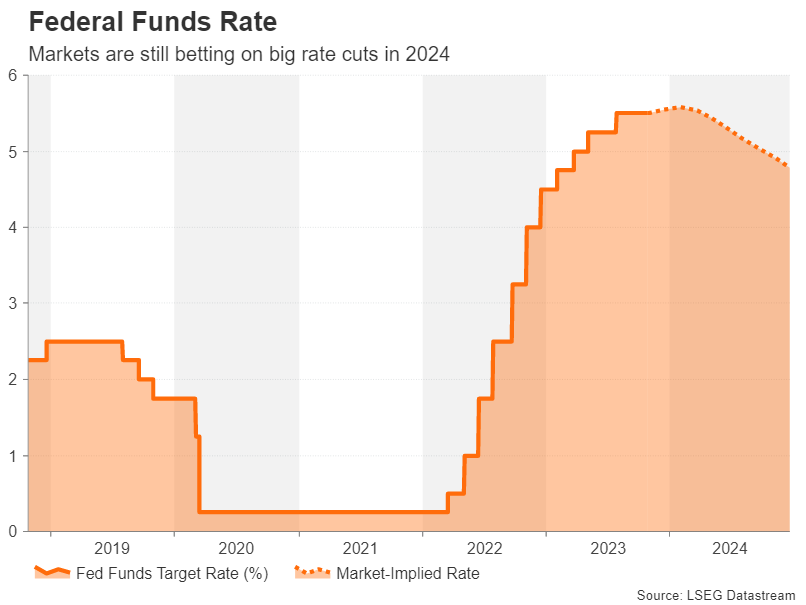

Fed pause likely to be of little relief for yields

Just a few weeks ago the November FOMC meeting was seen as a live one, but expectations of a rate hike have evaporated in the run up to Wednesday’s decision. The latest commentary from Fed officials has corroborated the markets’ view that the bar for further tightening is set quite high. However, as far as the Fed is concerned, it can be said that the bar for a rate cut has also been set very high. Investors have yet to be fully convinced by the higher for longer narrative even though the data supports the Fed’s version of the economy.

So as interest rates are kept on hold for the second straight meeting and in the absence of a new dot plot, investors will be hoping to get some insight on the rates outlook from Chair Powell’s press conference. In his last remarks before the meeting, Powell acknowledged that the tighter financial conditions from surging Treasury yields could lessen the need for further rate increases. But he also pointed out that if growth remains above trend and the labour market stays hot, the Fed may press the hike button again.

It’s unlikely that Powell will diverge much from those comments, although he may elaborate more on the impact of rising yields, which has the potential to spark some volatility should he allude that the Fed is done raising rates.

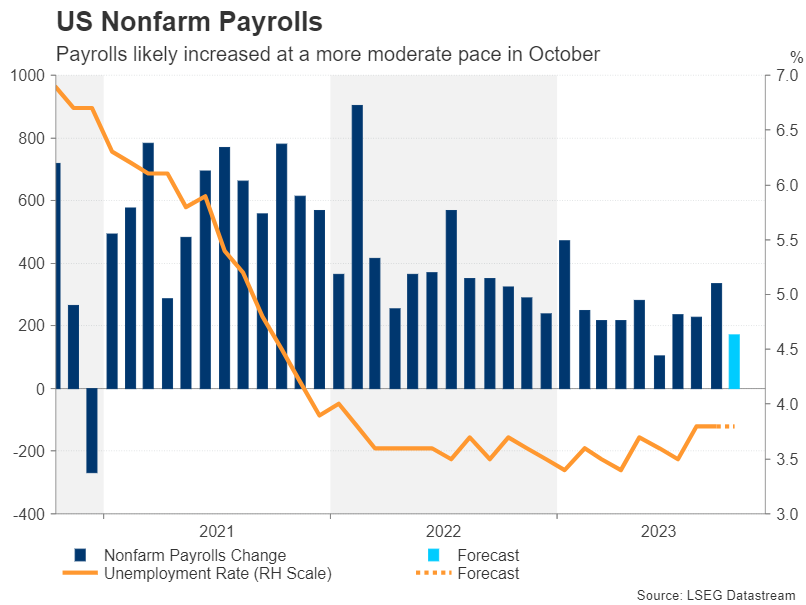

Will it be another hot jobs report?

But there’s also a risk that Powell may catch traders off guard again with his hawkishness, as US data keeps surprising to the upside, most recently with the advance GDP report. With a busy week lined up for US economic releases, it could be more of the same.

Quarterly wage numbers will be watched on Tuesday, along with the Chicago PMI and consumer confidence index. The ISM manufacturing PMI will be important on Wednesday. The JOLTS jobs openings for September are also due the same day, while on Thursday, factory orders might attract some attention after the very strong durable goods orders for September.

The real highlight, though, will be Friday’s nonfarm payrolls report as well as ISM’s non-manufacturing PMI. Following the shockingly strong 336k print for September, the October figure is predicted to come in a lot lower at 172k. But this would still be in line with a tight jobs market, especially for this late stage of the tightening cycle.

No change is expected for the unemployment rate, but earnings growth may accelerate slightly from 0.2% to 0.3% month-on-month.

Another solid report would likely add fuel to the rally in yields, potentially boosting the US dollar back towards the early October highs against a basket of currencies.

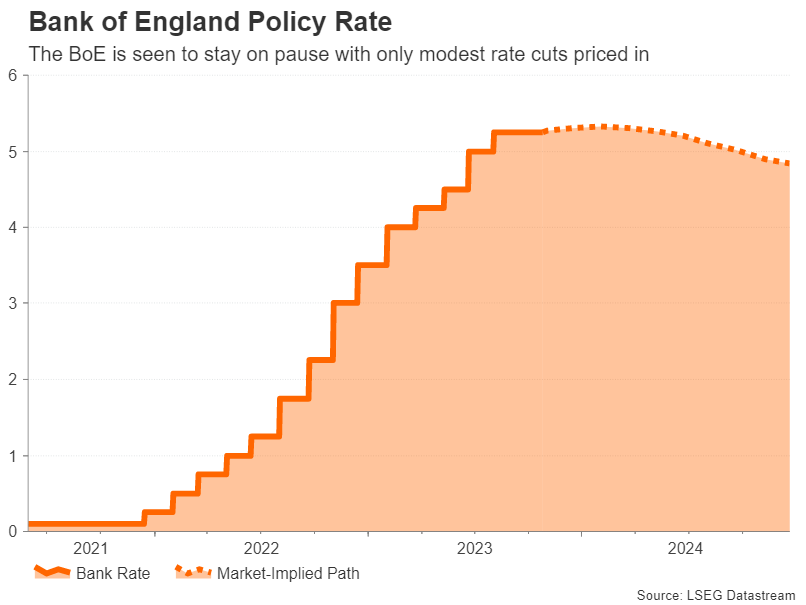

BoE pinning hopes on inflation drop

The Bank of England meets a day after the Fed on Thursday and it’s not expected to hike rates either. After the surprise pause in September, policymakers will probably hold firm on their decision to maintain rates at 5.25%.

The UK’s headline CPI rate unexpectedly held steady at 6.7% y/y in September, but the Bank is confident inflation will resume its decline in October when the new energy price cap came into effect. Hence, with inflation expected to fall sharply, unemployment edging higher and economic growth grinding to a halt, the BoE’s caution seems warranted.

Much of these downside risks have already been priced into sterling but some swings are possible depending on how gloomy or optimistic the BoE’s latest Monetary Policy Report is. When compared to the Fed or European Central Bank, investors see the BoE as being the least aggressive next year when it comes to projected rate cuts even as the economy flirts with a recession. Therefore, anything in the Bank’s forecasts that supports the higher for longer case might offer the pound some support.

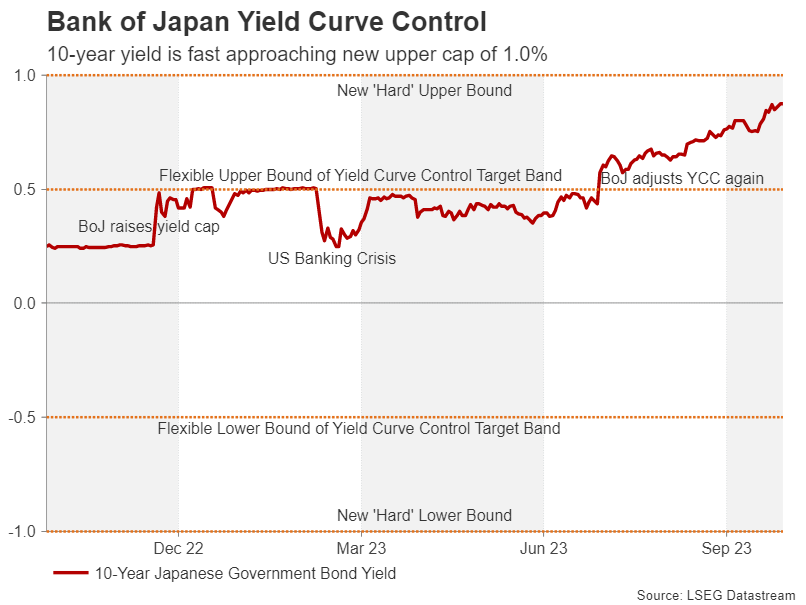

Will the BoJ come to the yen’s rescue?

With both the Fed and BoE set to stay on pause, the Bank of Japan meeting could be the week’s wildcard as there is growing speculation of a surprise policy tweak. According to local news reports, the BoJ is considering whether to raise the cap on the 10-year yield again after doubling it to 1.0% back in July.

Officially, the target band remains at plus or minus 0.5%, but it was tweaked to add some ‘flexibility’. But despite the creative language, there is little doubt the BoJ is well on its way to gradually winding down its ultra-accommodative policies as inflation in Japan has been running above 2% for some time now.

Even if price pressures have somewhat moderated in recent months, the Bank’s updated outlook report is expected to show that core CPI will overshoot the 2% target for the next two fiscal years, giving policymakers the green light to make further adjustments to the yield curve control policy. A relatively buoyant economy is another argument in favour of higher yields.

A further lifting of the yield cap above 1.0% would provide some much needed relief to the yen, which this week breached the 150 per dollar level. Whilst the move hasn’t prompted any intervention yet to defend the yen, the risk is that as long as Governor Ueda refuses to ditch his dovish rhetoric, any boost from a policy tweak would likely be limited.

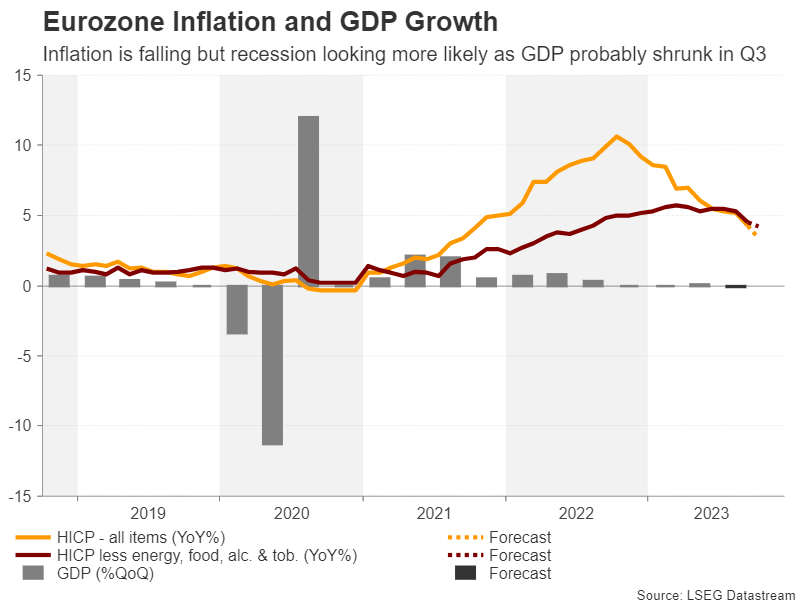

Euro on recession alert as GDP data incoming

The ECB gave its clearest indication yet that Eurozone rates have peaked even as President Lagarde declined to say this outright in her post-meeting press conference this week. But combined with worsening economic indicators and a resilient US economy, the euro is on the slide again and in danger of relinquishing control of the $1.05 handle.

It’s highly doubtful next week’s data will bring much cheer to the euro. The flash CPI readings for October are due on Tuesday, which will be released alongside the flash preliminary estimates of GDP growth in the third quarter.

Headline inflation is expected to have plunged from 4.3% to 3.4% y/y in October and the core measure that excludes all volatile items is forecast to have eased too.

The focus, though, will be on the GDP print, which is expected at -0.1% q/q, possibly signalling the start of a recession.

Can the loonie, aussie and kiwi halt their losses?

In Canada, weaker growth prospects have been weighing on the Bank of Canada’s mind too. Governor Tiff Macklem has hinted that further rate hikes are unlikely after the Bank kept rates steady this week, sending the loonie sharply lower.

Tuesday’s monthly GDP reading and Friday’s employment report for October are not anticipated to significantly alter the outlook for rates, possibly keeping the local dollar on the backfoot.

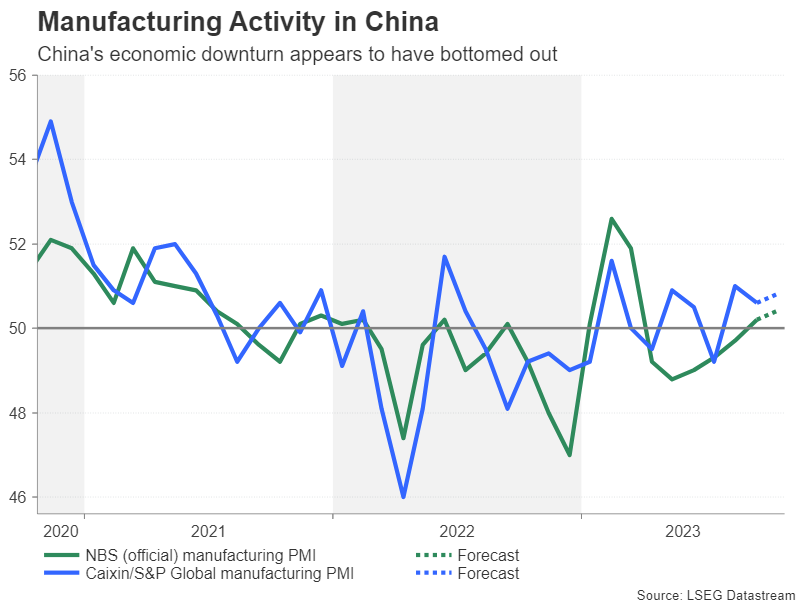

However, its aussie counterpart may receive a modest lift from Chinese PMI figures due on Tuesday and Wednesday should they point to improving sentiment in Australia’s largest export market.

Upbeat PMIs from China may also aid the New Zealand dollar, which has fallen to one-year lows. Kiwi traders will additionally be keeping an eye on New Zealand’s quarterly employment stats, starting with wage numbers on Wednesday and the jobless rate on Thursday.