A flurry of second-tier data releases in the United States this week will culminate on Friday with the all-important PCE inflation figures (12:30 GMT). Amid a very mixed picture on economic growth lately, the incoming gauges will be scrutinized closely. But ultimately, without any definitive red flags of an imminent recession, the best policy guide for Federal Reserve officials will be the core PCE price index. The US dollar stands ready to gain from any upbeat data following renewed jitters about Europe’s growth prospects.

A clouded outlook

Economic growth appears to be losing momentum on both sides of the Atlantic, although it is more pronounced in the euro area. Recession warnings have been sounding for some time now, but it’s hard to get an accurate read on the US economy. The downturn in the manufacturing sector appears to be deepening according to the latest PMIs by S&P Global but the slump in the housing market may be bottoming out. There is still no indication of a substantial cooling off in the red-hot labour market, which is encouraging consumers to keep on spending.

As things stand, it may take several more months for the fog to clear, hence why policymakers continue to fixate on sticky inflation as their primary concern, and on that front, Friday’s numbers are more likely to make the case for further rate increases this year than not.

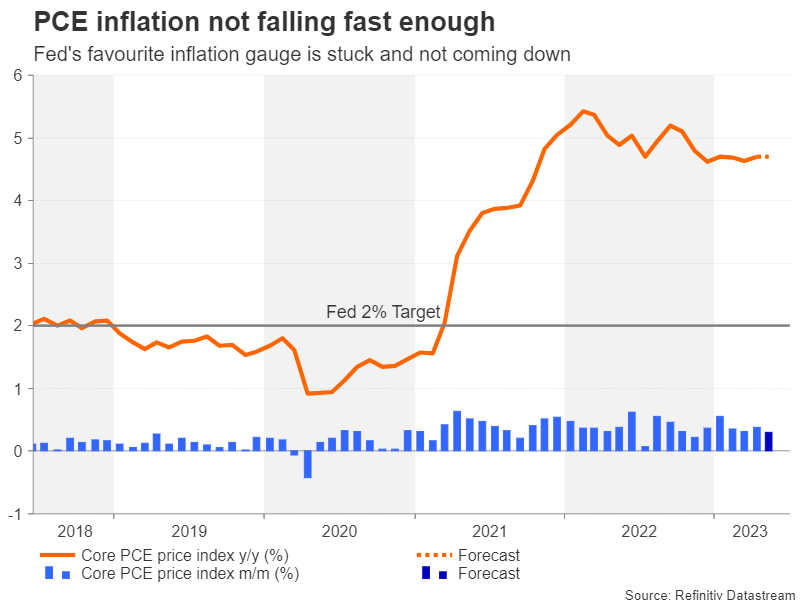

Will core PCE become unstuck?

The core PCE price index, which the Fed prefers to use for achieving its 2% inflation target, has been stuck between 4.6% and 4.7% all year and the flat trend isn’t about to change if the forecasts are to be believed. Expectations are that the core PCE price index was unchanged at 4.7% on a yearly basis in May, although the month-on-month rate is projected to have slowed slightly to 0.3%, which may please the Fed.

Personal consumption is also expected to have slowed, from 0.8% to 0.2% m/m in May, while personal income is forecast to have moderated marginally to 0.3% m/m.

Rate cuts bets are pared back

A day earlier, the final estimate of GDP growth in Q1 will likely get revised up slightly to 1.4%. The weekly jobless claims will also be important on Thursday amid somewhat higher numbers in recent weeks. The jobless claims provide a first look at how many people are applying for unemployment benefits. But even after the latest spikes, they remain at very healthy levels.

Thus, on the face of it, there are very few signs that the American economy is about to tip into recession, even after a cumulative 500 basis points of rate increases since 2022. This robustness is prompting many investors to think twice about betting on early rate cuts. However, market expectations remain hugely diverged from the Fed’s dot plot even after the latest repricing, and so, in the absence of a sharp drop in inflation or a surprise jump in unemployment, there are significant upside risks for the dollar in the medium term.

Dollar bulls refuse to go quietly

The euro’s advance against the greenback has stalled around the 50% Fibonacci retracement level of the 2021-2022 downtrend as the Eurozone recovery has stumbled and inflationary pressures in the region have started to dissipate, questioning the ECB’s resolve to hike rates a few more times this year. In the US, although inflation has come down considerably, it’s looking increasingly likely that it will need an extra nudge from the Fed to fall further, and the core PCE data may validate that view.

If the euro comes under fresh pressure on the back of a strong report on Friday, the 50-day moving average is the nearest support at $1.0873 that could defend against any declines. Should it be breached, the next critical region is likely to be between the 38.2% Fibonacci of $1.0609 and the 200-day moving average at $1.0572.

However, if the core PCE price index drops unexpectedly, the euro might manage to clear the 50% Fibonacci of $1.0942, after which, the $1.1075 area will attract interest again after the pair repeatedly failed to conquer it in April and May. A break higher would turn the spotlight on the 61.8% Fibonacci of $1.1274.

Banks in focus this week

In the bigger picture, the dollar has been consolidating against a basket of currencies for much of the year, mainly due to expectations of monetary policy divergence between the Fed and other central banks constantly swinging back and forth. The highly uncertain economic outlook is mostly to blame for this, but the banking turmoil also played a role.

The Fed will publish the results of its annual stress test on Wednesday, which are said to have been tougher this year, although the changes are unrelated to the strains in the banking sector and many smaller regional banks are not included. With the Fed’s post-banking crisis regulatory overhaul not due to be unveiled until later this summer, markets may cheer the stress test results as most banks are expected to pass with flying colours.