I went to Malaysia two weeks ago to hang out with my friend. He has been staying in Johor for a while and thought it would be a good idea for me to visit palm oil plantations near Kota Tinggi.

The thunderstorm in the afternoon kept us, two cats and one dog, in the house for a while. I took that opportunity to update him on the changes to the healthcare system and what they mean to his financial situation.

There have been changes to how our health insurance works. If you buy some shield plan and rider, you must co-pay about 5-10% of the bill. If you wish for a larger budget for cancer treatment, you will have to get a rider. A rider is not just to reduce out-of-pocket expenses in general anymore.

We then discuss whether he has a good plan if a major illness hits him today, tomorrow, 20 years from now, or 40 years from now, for a semi-financially independent person.

Knowing what I know, there are gaps in his coverage. He has an advanced-stage critical illness plan up to 65 years old. If a major illness hits him in the later years, that expense will come from his income portfolio for his daily living.

“How would I know if my income portfolio can provide for that? It sounds like it might be a big sum for a period!” He is right, and there are most likely trade-offs. Some of his daily spending will have to be cut down, and even then, how much are we talking about whenever that happens?

A solution for this is to buy a critical illness till 99 years old, but that is not foolproof, in my opinion. If you need a one-time lump sum of $70,000 today to alleviate your out-of-pocket cost, you could buy $100,000 of CI till 99 coverage.

40 years from now, would the nominal cost of what you need remain at $70,000?

If not, how much more insurance till 99 years old do you want to buy?

I shared with him that my personal plan is to supplement my current critical illness coverage with a medical sinking fund that will be provided when the critical illness coverage runs out.

I have written a personal note on this: $50,000 Portfolio to Supplement Lifetime Critical Illness Coverage.

A medical sinking fund for critical illness coverage is being very intentional in saving up for a costly sum that we would need later on in our life. By separating this from the rest of our financial goals, we can make sure that there is no double-counting and the money is there for us when we need it more or less.

While I was writing that personal note, I thought, why not do something extra and help him work out how much he needs today to supplement his existing CI coverage?

This post is to address his needs specifically but there may be parts of this that may prove useful for you.

What is Your Critical Illness Need Today?

If you face a severe critical illness event today, how much do you need?

This question will mess up a lot of people and it does mess me up enough. If you are not near retirement, or financially independent, or build up your wealth, the amount you need is make up of two parts:

- Replacing 3-5 years of your annual income or expenses so that you can quit your job and fight the illness well.

- A lump sum for out-of-pocket needs be it to alleviate costly alternative medical treatment, hiring care givers and other costs.

My friend is kind of financially independent, so number 1 is less of a concern. What he needs to figure out would be number 2.

I leave this up to him, but if he has no idea where to start, he can take a look at the breakdown of how I derive $74,000 in today’s money.

How the Medical Sinking Fund Works

So here is roughly the problem definition:

- My friend is currently 39 years old.

- He owns a $150,000 advanced-stage critical illness plan that covers him till 65 years old.

- No other plan.

I am going to let my friend figure out how much he needs today, but let us assume that my friend figured he needs a lump sum of $70,000 in today’s dollars.

I plot his existing insurance coverage against his CI needs in the chart below:

The $150,000 coverage is flat and will run out after 65 years old. Notice that the $70,000 needs to increase with inflation. I am using 3% p.a. in inflation for this $70,000. When my friend is 85 years old, the equivalent would be $272,653.

I wonder how many realize this flat payout and inflation medical needs problem.

So we are going to introduce a medical sinking fund.

This medical sinking fund:

- It is an investment portfolio.

- If you want to use an endowment, you can do so but do note that what drives the growth of either the portfolio or the endowment is the return of the underlying assets minus the cost. There is no magic to it.

- My conversation with my friend tells me he would use ISAC (iShares MSCI ACWI UCITS ETF using Interactive Brokers) but more on this later.

- The portfolio should grow over time.

- Any time you need it, sell off a portion or all of it to fund your medical needs.

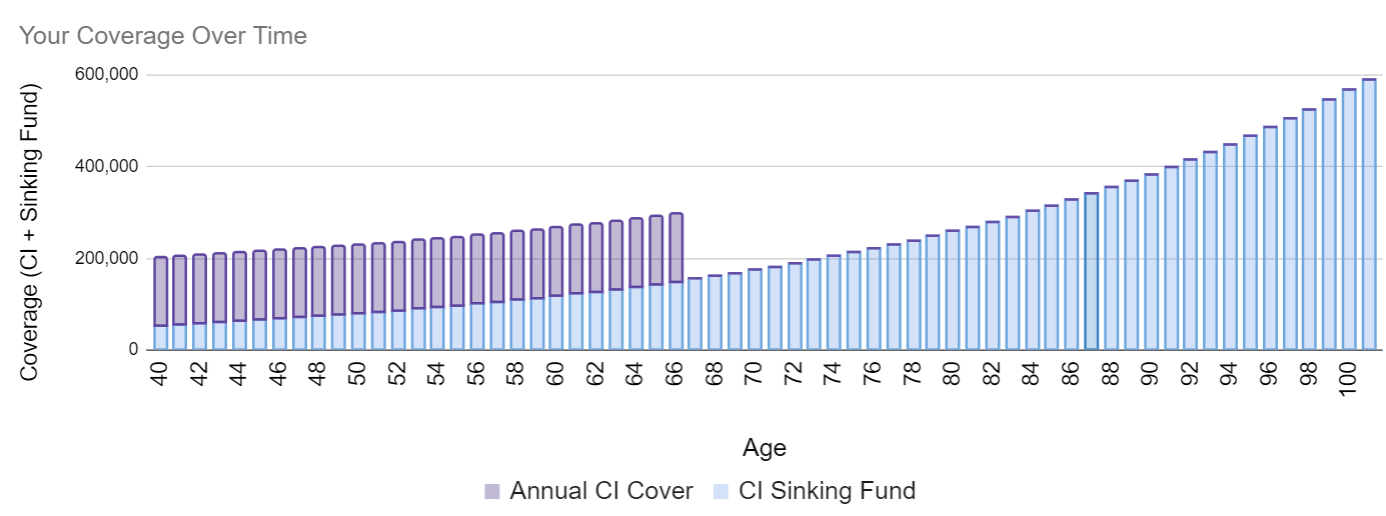

Here is how the portfolio value (CI Sinking Fund) and the insurance policy coverage stack up over the years:

I hope I don’t spell it wrongly as CI Stinking fund.

The value of the sinking fund grows over time. In this illustration, we are using a long term investment rate of return of 4% p.a. The coverage of the CI plan is stacked above (in purple).

The portfolio will have about 25 years to grow and capture the long-term returns.

So let us add back my friend’s CI Needs into the chart:

I could not do a stack column chart so that you guys can see it clearer.

We can see that all the light blue bars are higher than the purple line, indicating that if my friend needs the money at any point, there will be an inflation-adjusted lump sum for him.

The most delicate part is when my friend turns 65-66 years old. He would not have any CI coverage and the portfolio will have to be able to provide him with $155,490 (what the $70,000 is worth then). Therefore, you may wonder what happens when we don’t hit that return?

Now that I have explained the plan, let us try to discuss around the plan.

Planning Around Variable CI Needs, Healthcare Inflation and Investment Returns.

Look, it is very challenging to plan for a future that you and I would admit that is uncertain:

- We are not sure if the lump sum we plan for is enough. Did we missed out on some stuff or did we factor in too much stuff?

- There is a range of inflation of healthcare and non-healthcare needs.

- There is a range of investment returns.

I told my friend that if assuring major illness is such a big thing for him that he wants to make sure he has enough money to stand a fighting chance, then he should:

- Use a higher lump sum in planning.

- A higher long-term inflation rate.

- A lower investment return.

It will be a conservative plan but the flip side is that he will need to set aside a lot of money. Most likely he has to scavenge that from his income portfolio.

I came up with a table below for him to make his decision:

The table shows various minimum starting amount for the CI Sinking Fund depend on the CI Need today, healthcare inflation and investment rate of return.

For example if you plan for $100,000 and wish to plan with a conservative inflation rate of 4% and a 3% investment return, then you will need $190,000 in the Sinking fund today.

You will notice something: If the inflation rate is equal to the investment return, you basically need roughly the lump sum today. The investment return basically keeps pace with inflation.

I have also included a Multiplier so that you can roughly calculate if your CI Needs is not 70k, 100k or 150k.

For example, you notice that if inflation is 4% and the investment return is 6%, the multiplier is 0.6.

If you need $250,000 today, then the amount in your sinking fund is 250,000 x 0.60 = 150,000.

Using the Table in Reverse.

The nice thing about this table is that we can use it in reverse.

Suppose you would like to contribute $100,000 today.

What does contributing $100,000 means?

If we look at the table:

- CI needs $150,000 today if inflation is 4% and the investment rate of return is 6%.

- CI needs $100,000 today if inflation is 3% and the investment rate of return is 4%.

- CI needs $70,000 today if inflation is 3% and the investment rate of return is 3%.

- CI needs $70,000 today if inflation is 4% and the investment rate of return is 4%.

You can see the range of optimism and pessimism in your plan.

You could plan for $70,000 but there is a possibility you can have an equivalent of $150,000 today if the returns are good enough.

Setup the Portfolio For Higher Risk But Plan with a Conservative Rate of Return.

How risky is a portfolio that my friend can use?

The most significant consideration is whether he has enough runway to capture the return of a volatile portfolio. The worst equity sequence for the US market is that it spends 14 years of not earning anything. Which is a lower long term rate of return than 3% p.a.

My view is that to capture the return of a 100% equity portfolio, it is recommended that you should have 20-23 years between when you need the money and today.

In my friend’s case, that is 25-26 years away so he can invest in a 100% equity portfolio technically if he wishes to.

He can of course invest in a less volatile portfolio especially if his willingness to take risk is not so high.

A Medical Sinking Fund Tackles What-Ifs Better Because You Own the Power is In Your Hands.

If you buy a CI term or multi-pay CI term till 99 years old, you will pay a premium in exchange for someone to provide the sum when you need it.

That $100,000 or $200,000 is more certain than doing it on your own.

Most consumers are not sophisticated investors. I wonder how many even understand my sinking fund illustration and SSAC in the first place.

Even if they understand that part, they might not be convinced that they can earn the return 25 years from now. There is a body of work to complete to be convinced of the conviction of a broadly diversified equity and fixed-income portfolio.

And then… it would help if you had this capital in the first place.

Not many have the privilege to build this up, aside from their children’s university and their own retirement income plan.

A medical sinking fund is similar to your retirement income plan. Before you build your wealth, you buy term life insurance until age 65 in case you passed away and your dependents can live a normal life. After 65, you would have build up your retirement fund and your dependents don’t need you, or your wealth can be activated to help them.

Those with means would build up the medical sinking fund for a time you most need it.

Some may say that the equivalent of $70,000 years from now may not have accounted for something, but we can say the same for the CI insurance that you have planned for. Most of the arguments against the sinking fund exposes the CI insurance the same way.

The control for the sophisticated comes if you manage to earn a median return of 6-7% p.a. You have the power to manage the inflation-adjusted need and if you have a change of heart, you can reallocate your resources to other goals.

The money is fungible.

But if You Would like to Get Critical Illness Till 99…

If you have a different philosophy to my friend and me, there are term plans till 99 years old.

There are also multipay plans till 99 years old. Recently, there have also been LIMITED Pay TERM Plans!

If you are interested, you can always write into Havend, and my colleagues can take you through an InsureWell Assessment of your insurance needs. Let them know that you may be interested to shore up your critical illness needs.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

The post Sizing Up a Critical Illness Sinking Fund for a Singaporean Friend. appeared first on Investment Moats.