I had some content that I would like to talk about today, but one of our acquaintances shared with me the dispute of how a financial representative of JPMorgan Chase may have badly mismanaged Peter Doelger’s net worth.

Read JPMorgan is in a fight over its client’s lost $50 million fortune.

Peter Doelger’s net wealth was worth at least $50 million, but within the span of 5 years, they were under the advice of a financial representative; they ended up with $1.5 million and needed to sell their Boston condo and move in with relatives.

The Doelger family is suing JPMorgan, but JPMorgan also filed a counterclaim in the same lawsuit, saying their accusations have no merit and pressing them to pay the bank’s burgeoning legal costs.

The whole article exposes a lot of what he says and what the bank says. To complicate the matter, Peter Doelger had shown signs of cognitive decline at the time he signed an advice deviation waiver letter.

The contentious part of this lawsuit stems from whether:

- There is a breach of duty in providing sound, suited advice.

- Whether the bank went through with advice despite knowing that Mr Doelger is in cognitive decline.

- The suitability with what is recommended.

I was quite captivated by what was recommended:

- Mr Doelger’s portfolio is made up of pre-IPO shares in biotech companies, an MIT professor’s high-frequency trading fund, Korean real estate and municipal bonds. There is also securities in master limited partnerships, or MLPs focused on oil and gas.

- He first invested in the MLPs in 2009 through a Lehman Brothers subsidiary but JPMorgan became a custodian after Lehman’s collapse. JPM gave him a $6 million line of credit which he used part of it to ramp up his investments. From 2009 to 2014 the MLP outperform the market.

- While the returns swell, the debt to JPMorgan swell to $17 million.

- A JPM representative named James Baker tried to move this MLP portfolio to the bank by telling Mr Doelger about JPM’s new MLP program managed by Chickasaw Capital Management. This is where things get weird. When they tried to move the portfolio to the bank, James Baker send email saying Mr Doelger is worth $90-100 million and wanted to transfer $33 million worth of MLP to the program. I think the compliance seem to think it is not recommended to have more than 5% of their portfolio in MLP. And hence they got Mr Doelger to sign a “Big Boy Letter”, which is a letter stating you know what you are doing.

- Mr Doelger signed a letter upfront in 2015, attesting to his sophistication and interest (they are debating he has shown cognitive decline almost on the day he signed this letter) in making outsize, risky bets on oil and gas partnerships.

- JPMorgan repeatedly suggested to Mr Doelger to diversify and reduce his overall exposure.

- The wife, Yoon said these financial decisions were difficult for her and at times, when she check whether her husband knows what is going on, her husband said he does not understand what James Baker is saying.

- The MLPs after 2015 was turbulent and since they form a large part of the Doelger’s portfolio it became a problem. The loan at one point ballooned to $14 million but that was where the article got messy about the situation. There were periods where they were advised to pay down the loan. During COVID, everyone remember how the oil and gas was hit and the portfolio dropped $16 million in the first two months of the year. When Yoon sought James Baker for advise, he advise them to stay invested but things got more turbulent as there was a 24% fall in a single day and they were close to margin call. James Baker allegedly suggest to sell off $7.1 million to pay down the debt and assure the family that the portfolio can still generate $550,000 in annual income.

- As the market continue to tumble, the wife panic and sold the remaining assets to pay off their loans, which left $400k worth of MLP and $1.1 million in another account.

As someone working in advisory, I can take this article in a lot of different ways. I can say this is a good case study whether we are rebelling against something that will come at some point which is our cognitive decline. I could debate whether there is a breach in fiduciary duty of the JPM representative.

But what stood out to me the most was how their entire net wealth was setup.

The net wealth most likely started with cash and numerous properties. These are the staples of the ultra-high net worths. But their portfolio eventually became a zoo of many other disparate investments.

Who gave the idea of a HFT fund, IPO biotech stocks and…. MLP?

Someone definitely gave the idea to them, but the reason Mr Doelger eventually bought them was because either he understood them, or something in the sales pitch matches something Mr Doelger was looking for deep inside him.

And it is what is deeply inside him that might have crafted how weird this personal portfolio looked.

In this sales industry you can do it in two ways roughly:

- Know what people want deeply inside, and make a good case to appeal to them.

- Know what people want deeply inside, and if you know it is usually flawed, make a good case of a more sound plan and hope it appeal to them.

In my opinion, the second one is much harder.

The primary drivers of number 1 in my opinion are:

- Returns.

- A need for Income.

- Ego, appease curiosity, wishing for excitement.

How can MLPs form the primary basis of the portfolio? Because we think that returns is the most important. The great returns of the MLPs in the past is what made it easy to stick with them but as returns may be the SOLE reason of how they look at things, it makes it very difficult for them to diversify away.

The second big reason is that the MLPs throw out a good yield (not sure how the tax situation is managed but if that is taken care off, I assume they get a good income out of it).

Sometimes, I feel we can replace the 3 big local banks in MLPs and it would feels the same.

When your portfolio is very concentrated in a single kind of structure, in a specific sector, you live and die by that concentration. It did very well for the Doelgens until it doesn’t.

Many investors want the returns that come from the concentration but they only realize too late they cannot stomach the volatility and uncertainty that usually accompany these sector, regional or company concentration.

We can make a case that Ms Yoon the wife shouldn’t have panic sold but based on what was provided by the article, the right thing to do during period of higher volatility may be to not do rash things, which they were told. The time to act is before and after if I were to put on my timing hat.

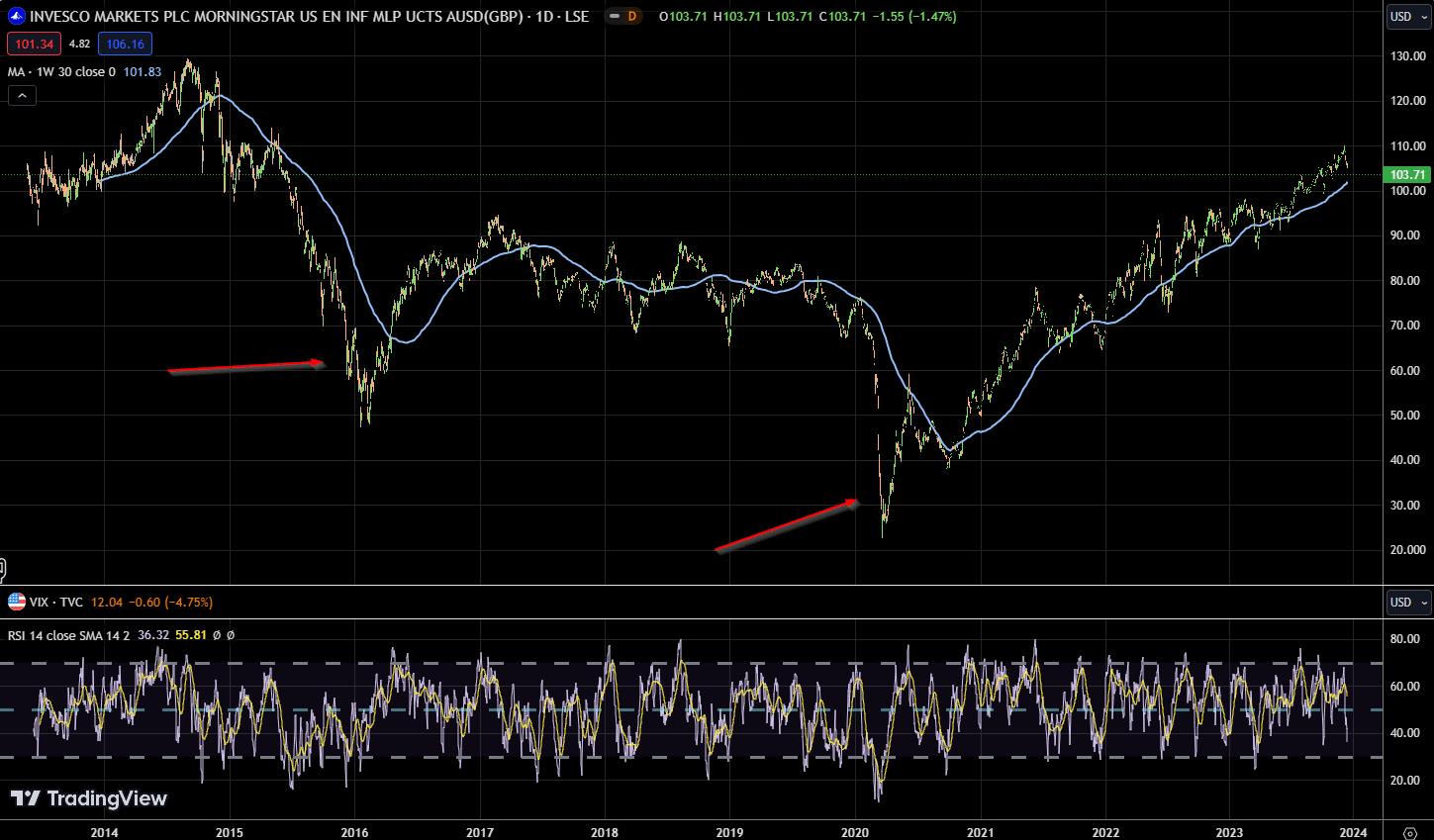

Personally, I hold a small position in one UCITS MLP with a ticker symbol MLPS. The chart below gave you some context the degree of volatility the Doelgen’s portfolio have to go through:

A big part of the downfall is due to: Leverage.

Leverage… unfortunately is a staple of private wealth investing.

I always wondered is it the bankers seducing the high net worth into taking more debt or deep down inside these high net worth, return on debt is very, very, very appealing to them.

Debt is like a monster they know can run wild. They think they are very smart, know the risks and can tame this monster to do their bidding.

But it always fxxks people up.

Many ultra high net worth came from being business owners. They build their wealth through taking calculated (or sometimes uncalculated but lucky) risks. They bring the same mentality to their wealth building.

The appeal of “Using other people’s money to make more money” is so strong.

The bankers may be blamed for seducing them by incepting the idea, but the clients have to find it appealing in the first place.

It is usually when they went through these ordeal then they take a step back and wondered:

Why am I taking so much risk by taking on leverage? Do I have to take on so much risk in the first place?

The truth is an assessment of their plan through sound lenses will tell us they don’t have to.

Years of sales representative stroking your ego, incepting seemingly great, foolproof strategies would setup an investment philosophy that will become much less compatible with your true financial goals.

Richer people might eventually realize that what they know deep inside may be flawed and hence they are open to explore what is the right way to look at investments or wealth management.

The financial representative may have much to blame but somehow, I feel investors in the end often get what they wanted. Just that what they want may not be really what they are truly looking for.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

The post It Takes Two Hands To Collapse a $50 Million Fortune. appeared first on Investment Moats.