Table of contents:

Quick Stock Overview

CATL by the numbers.

1. Executive Summary

A brief discussion of CATL and its potential appeal to investors.

2. Extended Summary

A more detailed explanation of CATL’s business and competitive position.

3. Powering the Electrification of China

A success story built on China’s push for electrification.

4. A Deeply Technical Company

How CATL’s culture led by engineers made it successful.

5. CATL’s Future

Technological breakthroughs create the next step of the company’s growth.

6. Financials

Exponential growth, massive investment, and a reasonable valuation.

7. Conclusion

Quick Stock Overview

Ticker: 300750.SZ

Source: Yahoo Finance

Key Data

| Industry | Batteries / Electric vehicles |

| Market Capitalization ($M) | 159,240 |

| Price to sales | 4.01 |

| Price to Free Cash Flow | – |

| Dividend yield | 0.15% |

| Sales ($M) | 39,674 |

| Free cash flow/share | – |

| P/E | 40 |

1. Executive Summary

Update: CATL’s latest quarterly results, reported on March 9, 2023, showed a 92.9% increase in net income and a 152% increase in revenue over the equivalent quarter in the previous year. The margin was 17.2%, and the Company controls a dominant 37% of the global EV battery market.

Electric vehicles (EVs) are a growing trend in Western countries, led by high-end car brands like Tesla and, more recently, Audi, General Motors, and many others. But the real EV revolution is happening somewhere else, in China.

With China representing by far the largest EV market, it is not surprising that the largest battery manufacturer in the world is from there as well.

Battery tech is an ultra-competitive sector. Any advance in battery chemistry allows for more range, safer design, and cheaper vehicles. This also means intense requirements for a high R&D budget and economies of scale to beat aggressive competitors.

By controlling 1/3 of the world market, CATL can reach a scale and capacity that none of its competitors can rival.

Its newest technology is truly groundbreaking and should usher a turn for EVs from expensive innovation to everyday life items, as it can greatly reduce the current limitations of EVs.

In parallel, CATL will be able to grow in other new markets, like grid-scale energy storage, other types of vehicles (delivery, trucks, ships), and battery recycling. It is also starting to produce outside of China, trying to capture the quickly growing European market.

The company has a lot of cash on hand and a reasonable debt load. It is also profitable and growing rapidly. While not cheaply valued, it is now priced at a much more reasonable level than it has been in years.

2. Extended Summary: Why CATL?

Powering the Electrification of China

CATL has emerged in less than a decade from a spin-off from a Japanese consortium to the company producing 1/3 of all lithium batteries made in the world.

Its initial success was built on the back of generous state subsidies, but it is now standing on its own.

A Deeply Technical Company

The company is atypical in China, focusing on R&D and innovation. Through its technical excellence, it has brought almost every car maker in the world onto its customer list.

Through a company culture of openness and operational excellence, CATL has been able to keep these relationships growing and become the world leader among battery manufacturers, beating its Korean (LG Chem), Japanese (Panasonic), and American (Tesla) competitors.

CATL’s Future

CATL’s R&D effort is paying off, and the company can now manufacture a revolutionary “million-mile” battery with twice the energy density of previous technology. This will accelerate the growth of the EV market and open new opportunities for trucks, ships, and utility-scale energy storage.

The company is also proactively adapting to looming metal shortages (lithium copper, cobalt, nickel) thanks to prescient investments upstream in the supply chain (mining, processing) and fully developed recycling processes.

Filling an EV Investment Gap

EV manufacturers have been the darlings of the investment community for several years, with valuations often soaring far beyond rational levels.

Today’s market is becoming increasingly challenging for EV makers. EV adoption is expanding rapidly, but large numbers of new companies and new models are entering the market, generating unprecedented competitive pressure. It remains unclear, for example, whether specialist EV makers can compete with the economies of scale that legacy automakers can bring to bear as they enter the EV market.

It’s not clear who will dominate the EV market, but CATL clearly dominates the battery market and is well-positioned to continue doing so. That could make CATL a better bet than any single EV maker.

Financials

Revenues and net income are growing at an accelerating pace. So are investments in R&D and CAPEX spending. The company’s balance sheet is very solid, with a massive amount of cash on hand and a reasonable debt load.

Valuation is not cheap, but not outrageous either, considering the growth profile. It is, in any case, a lot more sensible than at its peak in 2021, 50% above the current valuation.

This report first appeared on Stock Spotlight, our value investing newsletter. Subscribe now to get research, insight, and valuation of some of the most interesting and least-known companies on the market.

Subscribe today to join over 9,000 like-minded investors!

3. Powering the Electrification of China

From Humble Beginnings to Giant

CATL is a rather new company by today’s tech industry standards. Compared to Google or Amazon, founded in the 1990s, or even Tesla in 2003, the CATL foundation in 2011 is downright recent.

The company is a spin-off of Amperex Technology Limited (ATL), which produced batteries for small consumer electronics and was founded in 1999. CATL would go on to focus on electric car battery technology. ATL was incorporated into a Japanese consortium in 2005 and sold its last ownership in CATL in 2015.

From this early start, the company has grown into a key supplier of batteries for a very large array of car companies, including BMW, Daimler, Hyundai, Honda, Stellantis, Toyota, Volkswagen, Volvo, and – maybe the most spectacular achievement – Tesla, a company normally obsessed by vertical integration of its supply chain.

This impressive list does not even include the many Chinese car brands like BAIC, GAC Group, or Geely, less well-known in the West but still major contributors to global EV sales.

CATL is also unusual for being based away from the usual Hong Kong, Shenzhen, or Shanghai centers of operation of Chinese tech companies. It is still operating from Ningde, the hometown of ATL founder, Mr. Zeng.

Before becoming an entrepreneur, Zeng worked for a state-run company earning $30 USD a month. In 2021 Zeng became the second richest man in China, below Alibaba’s Jack Ma and ahead of ByteDance founder Zhang Yiming.

Ningde was a rather unremarkable coastal town, and even today, after tremendous growth and development, it is still home to “only” 3 million people, far from a big metropolis by Chinese standards. You can see the stunning growth of the city, almost entirely based on CATL’s success, in this QZ article.

It seems Zeng’s style fits his hometown, as his discretion and low profile have sometimes seen him called the “anti-Elon Musk.” Since earning a Ph.D. in condensed matter physics, his career and scientific work have been dedicated entirely to better battery technology. While many tech CEOs are mostly managers, I think it is fair to credit Zeng for the company’s track record in innovation.

Riding the Electric Subsidies

The success of CATL came partly from the usual sources of Chinese industrial companies’ success stories: cheap labor, very good engineering, and unrestricted and somewhat protected access to a 1.5 billion-person market.

But it would have gone differently without a massive push for vehicle electrification by the Chinese government. In 2008, the Chinese government mandated ATL for a fleet of prototype electric buses for the Olympic Games.

In the next few years, the government would launch a series of campaigns to promote research and development of electric vehicles. Perceiving an opportunity, Zeng left ATL and spun off CATL from it in 2011.

One part of the subsidies created the demand for this new market through public spending. For example, Shenzhen turned its entire fleet of 16,000 buses electric. The government also paid 1/3 of the EVs costs to the buyers.

And it worked. In 2022, 4 million of the new cars sold in China were EVs, and another 1.7 million were hybrids. This makes China a market 5x larger than the USA when it comes to “new-energy vehicles” (EV and hybrids). China is a bigger EV market than the rest of the world combined. And by 2030, 40 percent of vehicles sold in China will be electric.

Another part of the subsidies was cheap factory land, tax breaks, and other benefits for car manufacturers looking to produce EVs in China. The only requirement was to use batteries from a list of a dozen approved Chinese suppliers, including CATL.

But truly, when considering technical performance and production capacities, the choice boiled down to only two suppliers: BYD and CATL.

BYD had very good batteries, but as a car manufacturer, it was not interested in supplying competitors like BMW. Similarly, BMW was not keen on being dependent on its main competitors in China or providing it money to gain a competitive advantage in a field where German manufacturers were already lagging.

Today, BYD, which happened to have Warren Buffett among its investors, is the leading Chinese EV manufacturer, with 1.85 million cars sold in 2022. CATL dominates global EV battery sales.

The last key subsidies came from a steady supply of rare earth metals, a key component of batteries, and a supply chain largely under China’s control.

Standing on Its Own Legs

By 2018, the Chinese government was starting to feel that EV subsidies had become too costly. Besides, the technology was much more mature, and national champions like CATL and BYD were firmly established.

Subsidies were cut to almost zero by 2020, and competitors from Korean and Japanese battery makers were given much greater access to the Chinese market. For Chinese companies, this type of transition from subsidies and a protected market to a really free market can be rough or even deadly.

Luckily, CATL had planned for it. Leveraging now long-standing relationships with foreign auto manufacturers operating in the country, it was already growing its export markets quickly.

It also had established divisions in Western countries well before the local demand for batteries was mature enough to require them. Finally, the opening of the Shanghai Tesla factories allowed CATL to add the most valuable car company in the world to its client base, extending a deal to 2025.

CATL successfully transitioned from a protected national champion to an international company able to stand independently. As you can see below in the graph of the last ten years of CATL results, the end of subsidies did not hurt the company’s growth at all.

4. A Deeply Technical Company

A Scientist and Engineer-Led Culture

CATL’s founder was a scientist before being a businessman. The culture of the company he founded reflects that. From the beginning, CATL’s strategy has been to produce the best possible batteries, not necessarily the cheapest or the easiest to manufacture.

To achieve this, the company is spending as much as it can on R&D. For example, in 2017, the company spent 11% of its revenues on R&D, compared to just 6% for its competitor BYD.

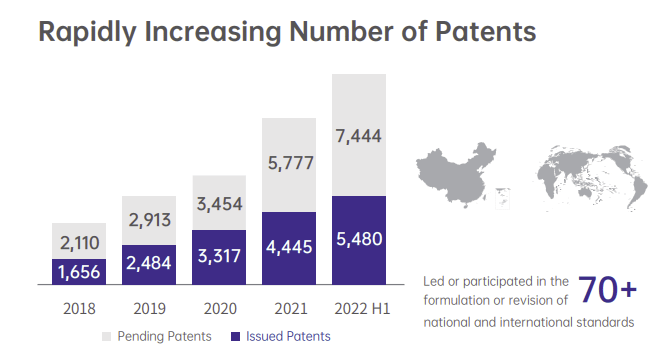

Many Chinese firms are accused of stealing IP or failing to really innovate, but CATL definitely does not fit this archetype. Instead, it is filling an exponentially growing number of patents and developing new battery chemistry that produces outstanding performance.

The other key aspect of the company’s culture is a very high level of openness. First to foreign talent, notably with the poaching from General Motors of an American battery expert, Bob Galyen, to make him the company CTO.

Secondly, this is a company that avoids putting its employees in “silos,” inspired by the success of Huawei with this strategy. Every employee should have multiple roles and understand several aspects of the company’s operation.

This creates a culture where initiative and problem-solving are rewarded and where open interactions between departments can improve daily operations.

I was hired as a supply-chain manager, but then they also made me program manager, and then also design-quality manager.

Staying at the Technological Edge

The focus on technical supremacy started with ATL producing lithium-ion batteries that would not swell or blow up, beating much larger companies like Sony at solving this problem. This also allowed the company to become the supplier of both Samsung and Apple when smartphones became a large market.

Batteries for EVs need to be custom designed for each car model. So by being early in the EV sector, CATL also learned to work with car manufacturers and adapt to their various technical requirements.

CATL can produce all possible types of batteries used in EVs, including cylindrical cells (Tesla), prismatic cells (BMW), or pouch cells (Jaguar). It uses two different types of batteries currently: lithium with nickel/cobalt/manganese for EVs (similar to smartphone batteries) and lithium iron phosphate for buses.

In just a few short years, CATL combined Japanese discipline, German engineering, and Chinese entrepreneurship to become one of the most desirable battery manufacturers in the world.

5. CATL’s Future

Beyond Lithium-Ion Batteries

The main constraint for EVs has always been the battery pack. From it come all the limitations of EVs compared to fuel-powered cars:

- Limited range and a lot of extra weight.

- Slow recharge, even with dedicated facilities.

- Risk of electrical fires that cannot be put out with water.

- Poor efficiency in cold weather.

- Higher prices than internal combustion cars.

- Somewhat short lifespan, often below the lifespan of the car itself.

Each of these issues has been a brake on EV adoption. Most of these problems can be reduced but not completely eliminated with traditional lithium-ion battery design. This is why researchers and battery companies have spent billions trying to find alternatives.

LFP

The first step for CATL was developing the best Lithium Ferro-Phosphate battery (LFP) in the industry. As I said before, these have already been commercialized by CATL for electric buses, which require more power than individual EVs.

LFP batteries have many advantages compared to lithium-ion.

- Cheaper.

- Higher safety (fire hazard).

- No cobalt, which is often sourced from Congo and produced with child labor.

- No nickel, which is often responsible for the high price of lithium-ion batteries.

- Much longer lifespan.

- Faster charging.

LFP was the design chosen by Tesla for some of its vehicles in a bid to reduce prices, fire hazards, and reputational risk from cobalt supply.

Currently, CATL offers LFP at $80/kW. This is below the $100/kW considered the threshold required for mass EV adoption.

CATL’s price advantage comes from a much cheaper cathode, 43% cheaper than other more energy-dense options. LG Chem and General Motors are working on their own version of this technology but are unlikely to achieve this cost level before 2025.

Still, LFPs are not perfect. They offer less energy density (energy per kilogram) than lithium-ion. So even if the total might be cheaper, you need more of them for the same results.

Essentially, CATL leadership in LFP allows it to stay dominant until the next step.

This next level was announced in 2020 when Zeng announced CATL would produce a “million-mile battery” jointly with Tesla.

The Million Mile Battery

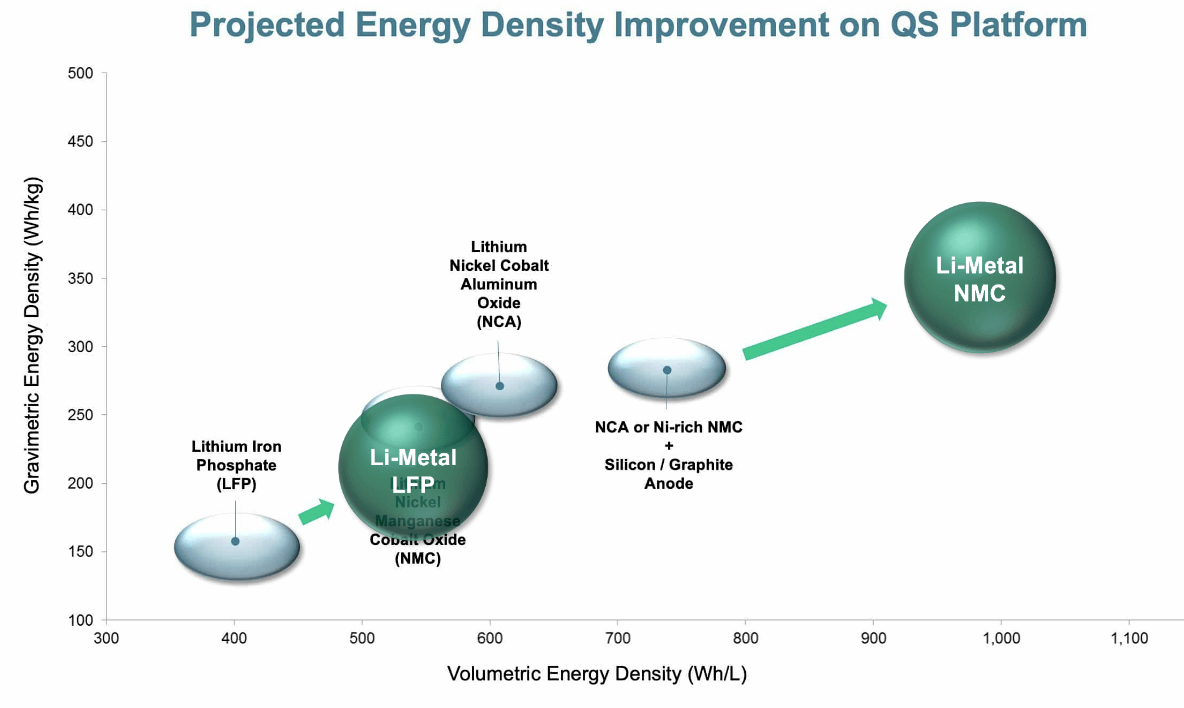

CATL’s LFP battery has a density of 200Wh/kg, up from 161 Wh/kg in 2020. This is good, but still not dense enough to produce cheaper and more efficient EVs.

Its new “million-mile” battery will not only be able to survive a million miles of usage (far more than most cars ever drive before turning into a rust bucket). It also has a battery cell density of 330 Wh/kg.

This near-doubling of density implies more than a doubling in efficiency. Batteries can represent up to half the weight of an EV: a Tesla Model S weighs 2130 kg (4697 lbs). By reducing the amount of battery needed, you reduce the total weight of the car. This reduces the amount of battery needed, which reduces the car’s weight, etc…

With the battery 32% of the total cost of an EV, reducing the battery needed by 60-70% means a huge cost advantage for manufacturers switching to the new CATL design.

Alternatively, it can offer a never-seen-before range of over 1,000 km for more pricey models.

And this is not all. This new design also has other advantages beyond costs (you can check CATL’s website for the details):

- much higher level of safety, even in case of a crash.

- low-viscosity electrolytes ensuring higher performance in cold weather.

- charging up to 80% in just 5 minutes.

- as mentioned before, a service life of 16 years or 2 million kilometers.

Overall, it seems CATL is on the way to keep growing its market share among battery volume, from the current 35% to potentially 40-60%. All this while the market itself grows quickly, driven by the costs saving CATL technology creates.

Currently, there are no serious competitors for the million-mile battery technology. The only serious alternative would be solid-state batteries, notably the one promoted by VW’s partner QuantumScape.

QuantumScape claims to have batteries reaching 550Wh/kg and even potentially 1100 Wh/kg. But these are, for now, just lab performances and have never been tested at scale.

Will this be an actual threat to CATL? Maybe. But for now, QuantumScape has been a lot slower than anticipated to bring its technology to a commercially viable scale. The transition from lab prototype to mass production is a difficult one. QuantumScape also has nothing even remotely close to the R&D and development resources that CATL has.

So this is something investors in CATL should keep an eye on but not lose sleep over.

Resources Shortages

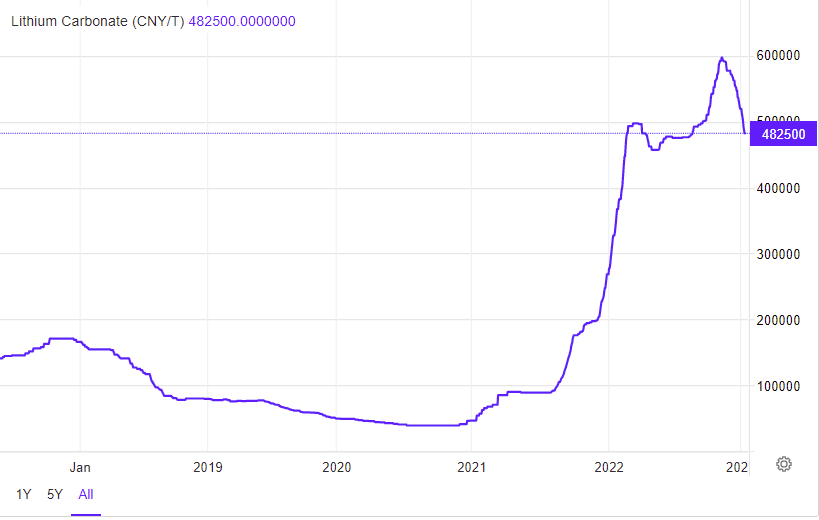

Speaking of risks, one that should also be mentioned is the cost of metals used to produce the batteries. Lithium, but also copper, cobalt, nickel, and other metals have all exploded in price in the last few years.

So while new technology like LFP or the million-mile battery can bypass the need for cobalt or nickel, the rise in the price of lithium and copper, most of the costs of a battery, is more concerning. CATL is, after all, as much a CAPEX, resource-heavy industrial company as it is a “tech” company.

The situation is also likely to continue, as investments in mining have been insufficient for several decades now, especially in copper.

According to a new report from Wood Mackenzie, the world will need 9.7 Mt of coper mine supply over the next decade from projects that have yet to be sanctioned, if it is to meet zero-carbon targets. “To date, a shortfall of this magnitude has never been overcome within a decade,” WoodMac’s copper researchers and analysts said.

Looming Copper Shortage Could Slow The Global Energy Transition

This is not a problem unique to CATL but to all battery and EV manufacturers.

Actually, CATL has been proactive in securing supply by investing massively overseas in the upstream part of the supply chain. Notably:

- A $5B lithium battery plant in Indonesia, starting in 2024.

- Investment in the Pilgangoora Lithium-Tantalum project, one of the world’s biggest lithium development projects.

- Lithium processing facilities in South Korea.

- Stakes in mining projects in Argentina’s lithium-rich region and in Congo (for cobalt).

The new million-mile battery should also help, as it requires less lithium than a normal battery, despite the improved performance.

Resource prices increasing might put pressure on CATL margins in the short term. But as its competitors are in the same situation or worse, this should not affect its dominant position. Denser and cheaper batteries, like the million-mile battery, could enhance that dominant position.

Beyond EVs

Other Vehicles

CATL’s destiny is currently tightly tied to EVs. That could change. Batteries are becoming increasingly important for other applications as well.

The first is other types of mobility, in which CATL’s experience in LFP batteries for buses will come handy. The rest of the world is yet to follow China in electrifying its bus networks.

The progressive electrification of truck freight should provide an extra market by the end of the decades. Even if this might prove quite slow, as the elusive and regularly postponed Tesla Semi truck seems to indicate.

Another way to improve electric vehicle potential is battery swap or battery as a service (BaaS). Instead of having users wait for the battery to recharge, they can just have it swapped for a new, fully charged one. This removes a problem for users (long waiting time for charging and queues at the charging station) and also removes the fear of the battery packaging badly.

Utility-Scale Energy Storage

Currently, CATL stationary energy storage solutions are used for two types of applications:

- Power backup for things like cell phone towers and data centers.

- Peak shaving batteries allow energy-intensive industries like cement producers to buy power when it is cheap (like at night) and use it later when power is expensive).

Renewable energy tends to produce at times when the electricity is not needed and not when it is. For example, solar panels do not produce in the peak consumption hours in the evening.

To handle this daily mismatch between demand and production, utility-scale battery systems will be needed if we want the electric grid to run on mostly renewable power. This represents an absolutely massive amount of storage, the equivalent of thousands or tens of thousands of EVs for every small town and the equivalent of millions of EV batteries for large cities.

CATL is the leader in these solutions, with 100+ projects worldwide.

I think this market will stay open for growth for CATL. I am not sure, however, that it will be the main driver of the company in 10+ years.

The reason is that lithium batteries are specifically designed to reach an optimal energy/mass ratio. This is great for vehicles.

But for utility-scale storage, a very small or very light battery is not critical. A very low price per kW of storage is. Weight or size is not really relevant when the battery never moves and can be stored next to a power station.

So other solutions should perform better, like Ambri’s liquid metal batteries, Redox Flow batteries, GMG Graphene Aluminium batteries, or Iron-Air batteries. They are all too bulky/heavy for transportation but might be 10x cheaper than lithium-based batteries when their technology is mature.

For this reason, I expect these technologies to beat lithium batteries for utility-scale energy storage solutions, at least in the long run. These are technologies where CATL would not necessarily have a competitive advantage.

Still, for the incoming decade, we can expect utility-scale batteries to be the driver of extra profits for CATL, even if not a sustainable business line.

Battery Recycling

The last activity that will grow for CATL is battery recycling. The EVs currently in circulation will be retired at some point in the future. Their batteries are both a valuable source of key minerals and an environmental/safety hazard.

Safe and clean recycling of batteries will be a necessary step for EVs to become the main transportation system in the world, especially with buses and trucks that will carry as many batteries as 20-40 cars per vehicle. And even more, volume, if other industries like shipping electrify as well.

CATL is already recycling 50% of the used batteries in China, or 120,000 tons, through its subsidiary Brunp, with a 99.3% recovery rate for manganese and cobalt. They do not communicate their recovery rate on lithium or copper, so I assume some progress is still needed there.

The recycling business should also help CATL to alleviate resource shortages by essentially mining old batteries.

It will also give CATL access to a VERY large pool of old EV batteries. These batteries can be either recycled or reused in utility-scale power banks. The second option is attractive, as a lower efficiency or capacity battery might not be fit anymore for use in EVs, but a much lower price could make reused EV batteries more competitive in the utility market.

US-China Relations

I cannot cover a Chinese company without mentioning the continuous degradation of relations between China and the USA.

This is part of a long trend that started with the Trump trade war. The escalations of more sanctions by the Biden administration, notably on the semiconductor industry, made it even worse.

The support of China for Russia in the context of the Ukraine war did not improve the situation either. Nor did the saber-rattling from both sides around the question of Taiwan’s independence.

So this is a risk to keep in mind when considering an investment in CATL. If the Ukraine war taught us something, it is that geopolitics can matter a lot when investing in countries that have a rivalry with the West.

I would, however, consider that CATL is less vulnerable than many other Chinese tech giants for a few reasons:

- The company is only listed on the Shenzhen stock market. This means you need a broker with access to this exchange to buy the stock. It also puts the company in a safe position if the US authorities use delisting as a tool to punish China and Chinese companies.

- There are no bases for a claim of CATL benefitting from Chinese subsidies and punishing it with tariffs. If anything, it is the West that is subsidizing EVs these days.

- European car manufacturers are a large part of CATL’s overseas business and will be less willing to sever ties than US car makers might have been.

- Batteries are a truly civilian application, and CATL has no links with the Chinese military-industrial complex, unlike Huawei, for example.

- There is no “national champion” equivalent to CATL in the West. Its main competitors are mostly Asian (LG Chem, Panasonic) or are already CATL partners (Tesla, BMW, Volkswagen).

So overall, I do not expect CATL to become the center of an international power game, at least as long as the US and China are not going toward a full-blown war. And then, I fear the CATL share price would be the least of our concerns.

Markets seem to agree to that as well, with CATL a lot less punished by the Chinese tech bubble popping than other companies like Alibaba.

On February 1, 2023, Reuters reported that CATL is considering listing its ADRs in Switzerland, with a listing contemplated as early as May. The offering would raise $5 billion that would be used to develop manufacturing facilities in Europe. The report relied on confidential sources and has not been confirmed by CATL.

6. Financials

CATL’s investor relation website is remarkably poor for such a large and international company. Its annual and quarterly reports are exclusively available in Chinese. So I relied on Yahoo Finance and Finbox.com data for this part of the analysis.

This is really something that should be fixed to increase the attractiveness of the shares to foreign investors.

At the same time, it really fits the company profile of being tech and business-driven rather than focused on share price fluctuation and financial markets.

Impressive Growth

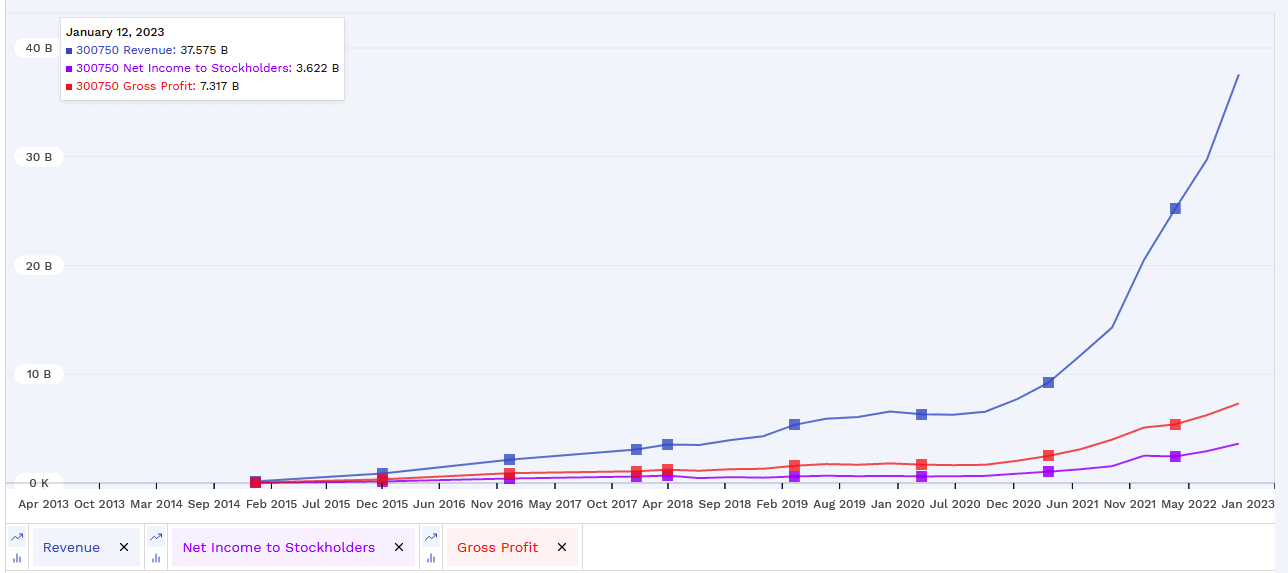

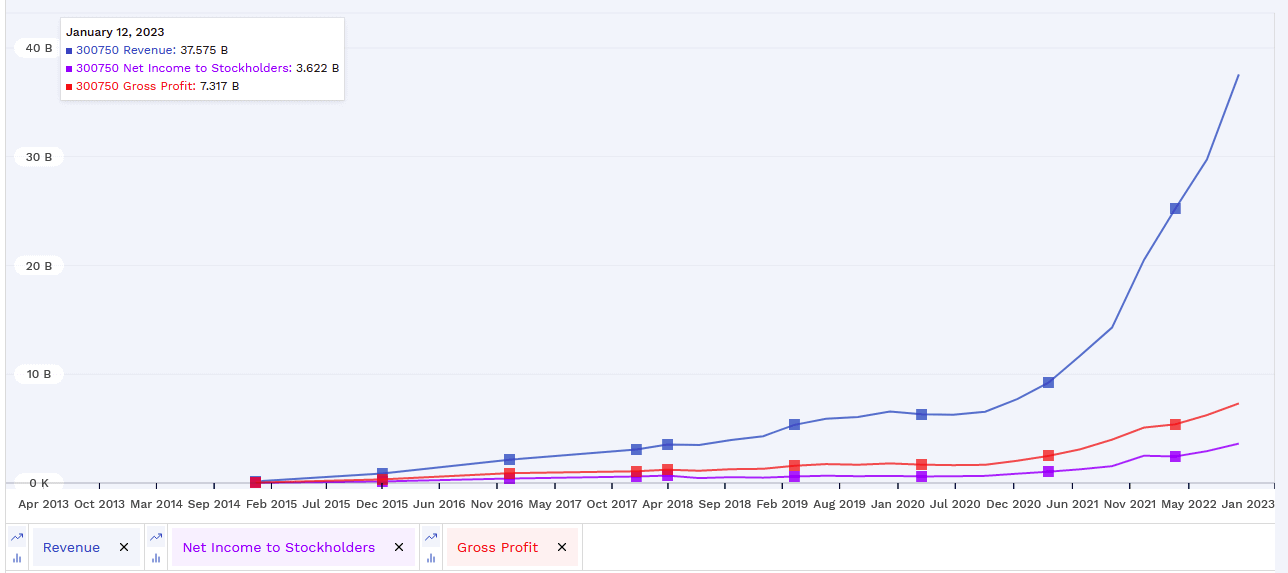

The end of Chinese EV subsidies in 2018-2020, followed by the pandemic, should have been a time of trouble for CATL. Judging by revenue, net income, or profit margin and gross profit, this was not the case. If anything, revenues have exploded upward since 2021.

Free Cash Flow & Spending

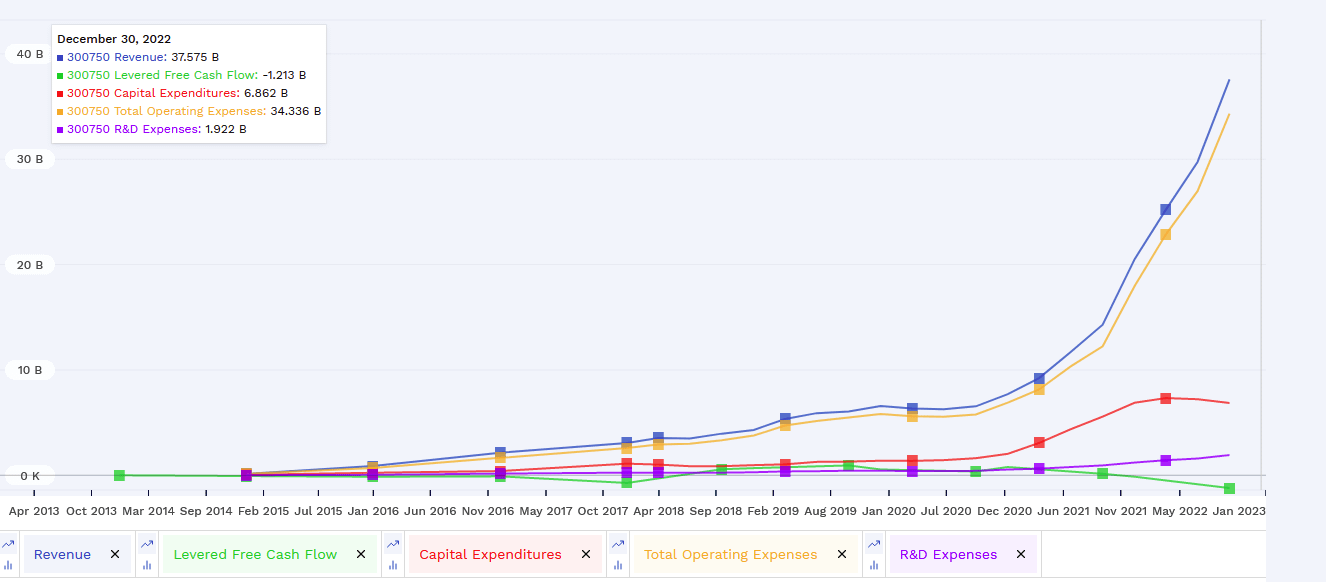

While net income is doing fine, free cash flow turned negative at the end of 2021. This was due to a massive CAPEX increase. The causes are many: general inflation, investments in the supply chain with mining and lithium refining, new factories to increase production, expansion in Europe with new production lines, and many large utility-scale projects initiated recently.

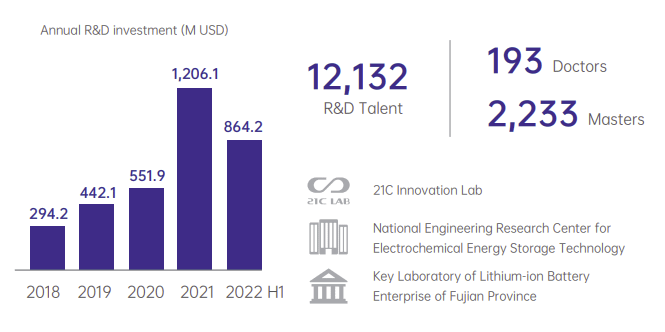

R&D spending has also gone from $430M in January 2020 to $1.9B in January 2023. This is a significant drag on cash flow but a necessary investment in the long-term health of the company.

With cash on hand at $18B and total debt of $8B, the company balance sheet is solid. Especially when considering an operating cash flow of $6B, in line with the whole CAPEX ($7B) and debt repayment ($2B).

At the current burn rate, the company can run nine years of operations, and would any solvability issue occurs, it could simply slow down a little on CAPEX and R&D spending to reach profitability.

Truly, it seems CATL has fully exited the stage of a growth company needing outside funds, except for a little debt to fund CAPEX. The large cash cushion also indicates that the company has anticipated higher rates and planned ahead to have all the cash it needs for future expansion and growth.

Valuation

With a P/E of 40, CATL is by no means undervalued. And this is even after a decline in the stock price of 50% since its peak in 2021 and revenues that have doubled over the same period.

So I would qualify at most the current valuation of reasonable. With little margin of safety, the only useful valuation tool is to judge if the expectations for future growth are reasonable. And I think the growth profile of the company is as good as it has ever been.

Revenues are growing at an impressive speed, actually quicker than ever.

The next step of growth should be triggered by the mass production of the million-mile battery design. This should have the effect of both increasing market penetration, but also drastically growing the market.

EVs have been able to penetrate the Chinese market at a much higher rate than in the West because the Chinese EVs were often for city travel, tolerating lower range, smaller cars, and lower performance.

With better batteries, EVs are now going to get not only greener but also cost and performance competitive with traditional cars. The arrival of an endless stream of new designs by almost every car brand will also push broader adoption.

Currently, the US sees only 5.8% of car sales being EV or hybrid. If this ratio jumps to 10% or 20%, we would still be far from fully electrifying the whole transportation network, but it would represent a colossal number of battery packs. The same if most Chinese cars turn electric.

The emergence of massive fleets of electrified buses, delivery vans, and even trucks will add to this massive demand for more and more batteries, likely stretching to the max the capacity of the industry to provide them. One bus can need as many batteries as tens of Teslas.

In that context, CATL’s large CAPEX spending today is the spare capacity to respond to its customer demand tomorrow.

Thanks to its R&D effort and the resulting superior technology, CATL is likely to size most of this growth in China, but also in the EU, USA, and Japan.

Returns to Shareholders

I would say that the decline in free cash flow is not alarming. It mostly reflects the need for rapid production growth and supply chain risk management. This, however, raises questions about when CATL will turn durably cash flow positive and be able to distribute some of its profit to its shareholders.

For the moment, it seems that CATL will stay focused on production growth, diversification in new markets, and exponential R&D spending to stay ahead of the competition. Considering its market and competitive position, this seems like the right call.

So most of the return should be expected in the shape of share prices rising up, something a lot less predictable in the short term than steady dividends. That’s also something to be expected for a growth tech stock.

7. Conclusion

CATL’s predecessor, ATL, was a classical Chinese industrial company. It leveraged cheap labor, good engineering, and low capital costs to build a durable competitive advantage and become a key supplier in the global value chain.

CATL is a different company altogether and has a profile that’s a lot less common among Chinese companies. The company is a true innovator on the level of Intel, GE, Panasonic, or Telsa. It has demonstrated brilliant corporate strategy, correctly anticipating the market’s future demands, the end of Chinese subsidies, and the looming shortage of battery metals.

It is also a global market leader, aiming for a quasi-monopoly position in its market through scale, best-in-class R&D, and a really prescient business strategy.

In that respect, I think CATL is emblematic of a new phase in China’s development, from being just a supplier of cheaper goods to a country able to imitate the American growth story, built on innovation and industrial prowess.

So short of out of control tensions between the two countries and a full-blown new Cold War, I think CATL could provide great returns for Western investors in the future.

It could even become one of the first Chinese companies with a valuation durably above the trillion dollar mark, joining the very short list of tech giants that became world leaders in innovation.

Holdings Disclosure

Neither I nor anyone else associated with this website has a position in CATL or plans to initiate any positions within 72 hours of this publication.

I wrote this article myself, and it expresses my own personal views and opinions. I am not receiving compensation from, nor do I have a business relationship with any company whose stock is mentioned in this article.

Legal Disclaimer

None of the writers or contributors of FinMasters are registered investment advisors, brokers/dealers, securities brokers, or financial planners. This article is being provided for informational and educational purposes only and on the condition that it will not form a primary basis for any investment decision.

The views about companies and their securities expressed in this article reflect the personal opinions of the individual analyst. They do not represent the opinions of Vertigo Studio SA (publishers of FinMasters) on whether to buy, sell or hold shares of any particular stock.

None of the information in our articles is intended as investment advice, as an offer or solicitation of an offer to buy or sell, or as a recommendation, endorsement, or sponsorship of any security, company, or fund. The information is general in nature and is not specific to you.

Vertigo Studio SA is not responsible and cannot be held liable for any investment decision made by you. Before using any article’s information to make an investment decision, you should seek the advice of a qualified and registered securities professional and undertake your own due diligence.

We did not receive compensation from any companies whose stock is mentioned here. No part of the writer’s compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed in this article.

The post Contemporary Amperex Technology Co. (CATL – 300750.SZ) Stock Analysis appeared first on FinMasters.