No-Penalty CD 4.90% APY for 11 months if you want to ratchet up. Platinum Savings now up to 4.95% APY. CIT Bank (not to be confused with Citi Bank) is an online-only bank that I keep open and going back to due to their multi-year history of competitive rates. They have a checking account, but their specialty is a variety of savings and CD products with high interest rates. I use their No-Penalty CD regularly for maximum optionality while maintaining a high interest rate (details below). Here are the highlights:

- 11-Month No-Penalty CD at 4.90% APY with $1,000 minimum to open. The 11-month CD keeps a fixed rate, but has no withdrawal penalty seven days or later after funds have been received. This means (1) high rate now, (2) interest rate will never go down during the term, (3) interest rate can still go up, and (4) all funds stay fully liquid. (If you have an existing No Penalty CD that you want to close and open up a new one, please see my instructions below.)

- (NEW) Platinum Savings Account at 4.95% APY if you maintain a $5,000 daily balance or higher. 0.25% APY if your daily balance is under $5,000. No monthly fees. If you have any other savings accounts at CIT and can meet the minimum balance, you should consider moving funds over to this account.

- Savings Connect Account at 4.60% APY if you open with $100. No minimum balance and no monthly fees.

- 6-month Term CD 5.00% APY, 18-month Term CD at 4.60% APY, 13-month Term CD at 4.65% APY.

Check out my rate chaser calculator to see if it makes sense for you to move money over.

New customer? Opening process overview. Here’s my review of the opening process if you are a new customer.

- The application process was completely online. You provide the usual personal information.

- You must submit to a credit check, but in my experience it was a “soft” pull which did not harm my credit. None of my various credit monitoring services showed it was a hard pull.

- You may fund via (1) electronic ACH transfer, (2) wire transfer, (3) mobile check deposit via CIT Bank mobile app (iOS and Android), and (4) mailing in a paper check. There was no option for credit card funding. I picked online ACH funding and you need to provide routing and account numbers, followed by manual verification via micro-deposits after a day or two. There was no instant linking option via login information.

After deposit verification, then your funding will go through.

You have successfully verified your external account. Please allow up to 5 business days for your funds to appear in your CIT Bank account.

No further action is required for this account. Thank you!

Existing savings or money market customer? Check your rate. If you already have an existing High Yield Savings account, it may remain at a lower interest rate than this money market account. If so, take a minute and upgrade yourself to the better interest rate. Click on “Open an Account” here, then “I have a CIT Bank account”, and then login with your username/password. You can do everything online and even fund your new Money Market account with an instant transfer from your existing Premier High Yield Savings. I wish I didn’t have to do this, but at least it literally only took a minute to complete.

How to transfer your money from an existing No Penalty CD into an new, higher-rate No Penalty CD (or any other new account). You have the option of moving the funds (with no penalty of course) over to a new CD with a new 11-month holding period if the current rate is higher than your existing rate. Here’s the easiest way to do so:

- Start a new online application for the 11-Month No-Penalty CD. Click on “Get Started” and sign-in as an existing CIT customer.

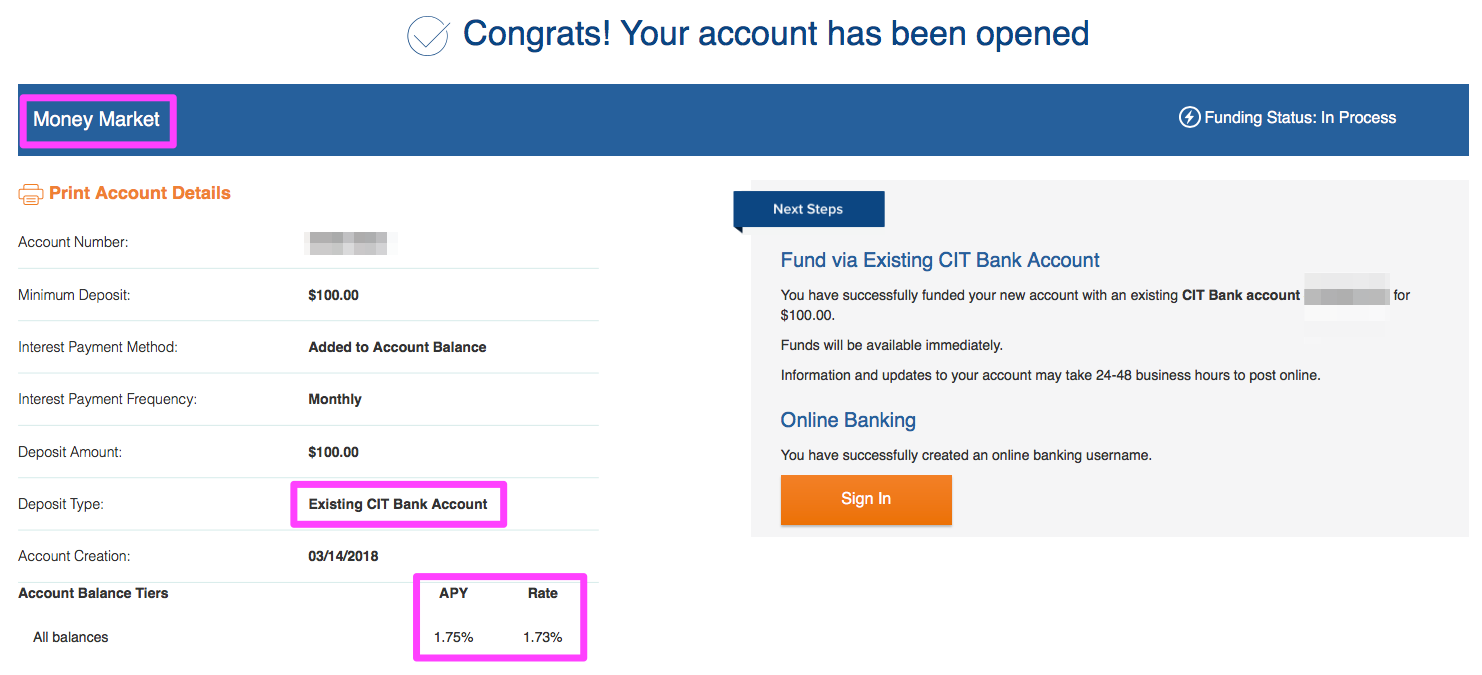

- After signing in, go through the opening process but look for “Existing CIT Bank Account” under “Funding Source”. You should see a list of your existing accounts, including any No Penalty CDs. (Screenshot below.)

- Note that online, your only option will be to have the entire CD balance (including accrued interest) moved over into the new CD. If you want a different amount, you’ll have to call CIT Bank customer service at 855-462-2652, open M-F 8a-9p ET, Sat 9a-5p ET, Sun 11a-4p ET. Press “0” for operator. Tell them you opened up a new No Penalty CD and you wish to fund it by closing out your old No Penalty CD.

- That’s it. The online option says it will take 2-3 business days to complete. Your new accounts will show up online.

User interface. While the front-facing website is pretty slick, after you login the backend is run by Fidelity National Information Services (subdomain ibanking-services.com). This is a popular backend software system used by many smaller banks and credit unions who don’t want to create their own software from scratch. It is better than before, but remains more functional than flashy. Similar story with the iOS/Android app.

Bottom line. CIT Bank is a lean bank offering targeted products for folks looking to get higher interest rates on their cash balances. They don’t maintain physical bank branches or fancy apps. However, I have been pleasantly satisfied with their customer service on my accounts with them. Their most compelling products are their Platinum Savings accounts, 11-month No Penalty CD, and often they have a competitive rate on at least one of their Term CDs. The No Penalty CD is unique in that you are always able to move out to a higher rate, even within CIT bank itself, all while maintaining a floor if rates drop (yes, it is still possible for rates to drop!).

“The editorial content here is not provided by any of the companies mentioned, and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are the author’s alone. This email may contain links through which we are compensated when you click on or are approved for offers.”

CIT Bank Review: 11-Month No Penalty CD 4.90% APY, Platinum Savings up to 4.95% APY, 6-Month 5.00% APY from My Money Blog.

Copyright © 2004-2022 MyMoneyBlog.com. All Rights Reserved. Do not re-syndicate without permission.