Our whole company had our “introduction to pickleball” session this morning.

Pickleball was the poison chosen by our company’s culture planning community to keep us cohesive and to help emphasize certain aspects of our culture we should deepen this year.

Having a “strong mind” was one of those.

I certainly need to have a strong mind after a whole morning of running around, bending to pick up balls and then having to be the note-taker for this year’s Singapore budget.

Finance Minister Lawrence Wong woke up on Friday morning with a different idea.

He chose violence and decided to nuke the CPF Special Account for those CPF members who are 55 years old and older.

My CEO, Chris, thought this wasn’t that big of a change.

You should see the meltdown in the 1M65 Telegram group.

My colleague Choong Hwee and myself were both moderators there, but we had to concentrate on listening to the budget. Before you know it, his unread 1M65 messages zoomed up to 1000+.

My CEO couldn’t have been more wrong. So many rich people with so much money that they want to shield or have already shielded in their CPF SA are so unhappy! It is as if the government suddenly announced that all your freehold property is now a 99-year leasehold.

After 1 day, I had more time to digest most of the announcements during the Singapore Budget and I think this CPF change is kinda big enough for me to reflect more upon it.

This would technically affect the planning of our clients in some ways and some work will eventually route back to me. The caveat is that whatever I post here is my own views not that of Providend, or now Havend , where I technically work for.

Here are my short thoughts (I want to go back to resting and not doing anything).

Two Related Announcements that Should be Considered Together

Mr Lawrence Wong announced that

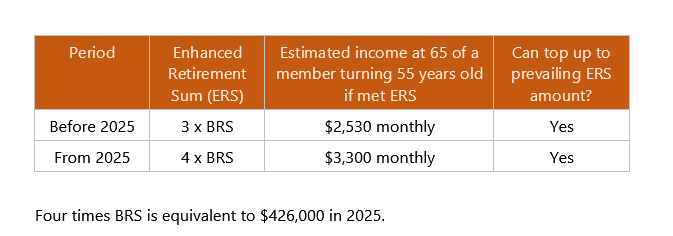

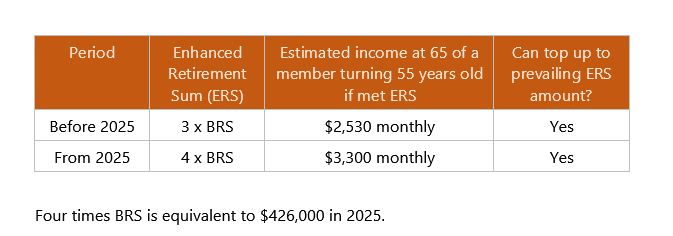

- They are raising the CPF Enhanced Retirement Sum (ERS) from 3 times the CPF Basic Retirement Sum (BRS) to 4 times.

- They will be closing the CPF Member’s CPF Special Account (SA) after the member turns 55 years old. The money accumulated in the CPF SA will go to:

- The money will be allocated to your CPF Retirement Account (RA) to meet the CPF Full Retirement Sum (FRS), which for example comes up to $213,000 for those who turned 55 year old in 2025.

- The rest will be allocated to your CPF OA.

- Then the CPF SA will be close.

A good way to understand this is to watch this video created by CPF:

By default, the government want us to accumulate enough in our CPF so that we can have enough income for our retirement. This is why they set this CPF FRS.

For those who don’t wish to put so much into their CPF LIFE or have prudently secured a home that is long enough relative to your survival (in their dictionary, it is about 95 years old), then you can just set aside half (CPF BRS) in their RA.

However, for those who felt that they need more income, the government allow them to top up their CPF RA with cash, or transfer from their OA to this CPF ERS sum.

In the past, members can only top up their RA to 3 x BRS but with this change you can top up more.

Not just that, but you can top up to the PREVAILING ERS and not the ERS for your 55-year-old cohort.

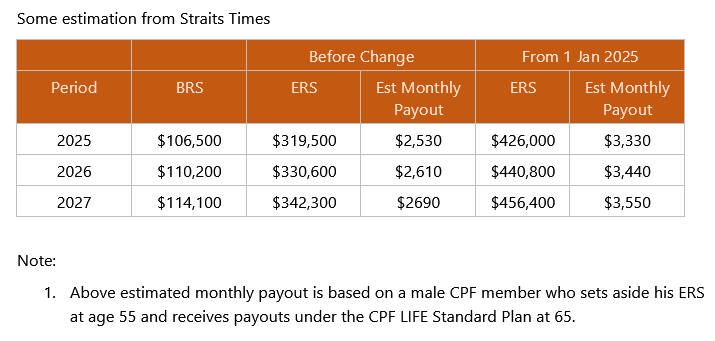

What this means is that when the ERS moved up from $426k in 2025 to $456k, you can top up your CPF RA to $456k.

So why do want to do that?

Eventually, the CPF LIFE will provide an annuity income for life for our needs. The table above is taken from the Straits Times and will give you an illustration just how much income that can be bumped up.

People forget about the Big Objective of the CPF

We can quite easily be lost in the noise and in the midst of all this, people forget that a key objective is to help CPF members take care of their retirement income needs.

CPF LIFE Annuity, as an income stream is unique in that:

- It is administered by our government entity.

- Pooled a group of people together therefore able to achieve additional income that otherwise hard to structure. As of today, I don’t know of any other financial income structure that does this in Singapore.

- Provide an income to hedged your longevity risk. This means that we are not sure how long you live, but this income stream will be there.

- Has probably the highest income to capital ratio out there. This yield can go up to 6% or 4%+, depending on your age and which scheme you chose. This means you put in less capital but get more income.

- There is an obligation to pay a relatively consistent income (while not guaranteed)

- They abstract investment volatility away from the members.

Many felt that they have a good solution that is even better than this configuration add together.

I have studied a lot of different income strategies and I find it extremely challenging to have the characteristics above. (If you got something that has a lot of these characteristics, do private message me about it).

With this change, the government have helped us immensely.

Typically, with these income characteristics, planners will match this income to the spending that is rather inflexible, long tenor and most important to the clients.

With this expanded ERS, it will greatly help our high net wealth clients who are planning for their retirement needs. Majority of their income needs is high and a higher CPF LIFE can help them match their spending that are essential and inflexible.

I am not sure how obvious this is but I do think that if a person I speak to cannot see this as a positive from Singapore Budget 2024 announcement, this person don’t know what he is investing for, or is not a very good planner.

People are Unhappy About Losing a Non-volatile Value High Yield Savings Account.

Currently, the money in your CPF SA earns 4.08% p.a. interest compare to CPF OA, which earns 2.5% p.a.

There is this technique called SA Shielding.

By default, when a member turns 55, CPF will automatically try to transfer whatever money you have in your CPF SA to your RA account, and if that is not enough to fulfill the FRS or BRS, they will transfer the CPF OA money. This means that your CPF SA, which earns a higher interest, is emptied first.

So this SA Shielding basically:

- Invest the money in your CPF SA, less the first $40,000 which cannot be invested, and top-up monies from RSTU.

- When the member turns 55, the first $40,000 from SA goes over to RA, while the remainder the CPF will take from OA. (It should be noted that you can shield your CPF OA if you wish to as well).

- After 55, you can then sell your investments and the money will earn about 1.5% more than if it is in the OA

And because you do not face the prospect of capital value volatility, this makes your CPF OA + SA really attractive.

With the closure of the CPF SA for a member after 55, their CPF OA savings account became nerfed.

You see people losing their marbles basically.

This comment I see in 1M65 really takes the cake:

Can we replace our MPs with AI bots then since they promote high tech n frankly speaking no one opposes to the rule change then what for we have MPs? Might as well have some ministers n all AI bots as MP’s since they also intelligent enuf.. n save some $$ for SG to spend on infrastructure n help the poors?

It is Interesting How People’s Fear Manifest Itself

I wonder if we should call it rich people’s fear.

I still know of people who deeply suspect the establishment and would try to take out money once they turn 55.

They will ask me questions about these CPF process just to get things right and what I uncover is that these people still exist.

Yet, you have people unhappy of not being able to put more money, or put longer into it.

CPF LIFE and many of these schemes are supposed to take care of those in the 2nd quintile of Singaporeans but over time, perhaps many feel that CPF is supposed to serve themselves and many Singaporeans are becoming more affluent. Part of this change to the ERS is to aid the affluent.

But their anger is manufactured by their fear they cannot find something as good as the CPF SA (I talked about why it is such a good account).

I wonder what is next? Retaliation?

In the past, I shared that each of us have this ladder of trust in which wealth building strategy or instruments we would rely on. Salary from our work usually is the top ranking follow by something else.

For some, they must have thought that this CPF SA would be one of the most highly ranked after their salary. You can then understand the anger that when this is removed, they are at “a loss” because their next ranking income or investment strategy ranks so low they don’t have conviction with the strategy.

For some, like myself or others, we learn about, try, and get comfortable with a couple of investing and income strategies that a CPF SA account doesn’t really rank high in our mind of the strategies we trust.

So when news like these hit, we lost an option but it doesn’t affect our lives so much.

Perhaps some can take this as a good time to learn to invest in risky assets. I would probably expand upon this in another point.

Is a 1.5% p.a. in Interest Difference So Significant?

I think this varies from person to person. Indirectly, the anger may show how much most Singaporeans struggle with investing to achieve a consistent return of 4% p.a. on their investments.

If not, some folks don’t really know what they fear or are scared about.

I can empathize with the struggle for those who don’t have the time to upskill and learn to build wealth with other strategies. I can also empathize with those requiring

But the oddest to me is seeing some people who have been prominently advocating investing in some risk assets they trust a lot cry father, cry mother over this.

If you have a so-call strategy that have high degree of certainty, making up 1.5% p.a. shouldn’t be a problem for your risk-asst based strategy.

Unless they:

- Have a poor understanding of wealth management.

- Doesn’t trust the investment recipe that they are trying to sell (or heaven forbid, they don’t understand their strategy that well)

- Just trying to rile people up.

After 55, Your Money is Liquid Already. You can reallocate your Financial Resources the Way You Desire.

Of course, some complain that, once again, the government has decided to change the rules. Therefore, we should be wary about the CPF.

Well, the newsflash is that the CPF Rules have been changing so often, but why the big complaint from some now? Is it because it goes against them and that is why it matters now?

People are just going to keep complaining.

Many are just selfish enough that the system should only work in a way that works for them and not in any other ways.

I find most complain to be weak in this case.

You got to realize it is after the member turn to 55-years old.

You can take out the money, above the CPF FRS.

You do not have to transfer to your RA.

If you felt the returns in CPF are low and you could do better, then by all means, you have free reign how you use the money.

Would this cause people to take the money and go Siam Dius? The people who needs money to go Siam Dius would have kept the minimum in CPF at 55 even under the current rules.

There is no difference with this change. Those who wish to keep the money in CPF is of a certain mindset and seldom change so fast.

Whether you can shield your money currently, or if you couldn’t in 2025, you have a responsibility to your family to deploy your wealth well and you always have a relatively restriction-free way to do this.

If Policy Risk is So High, Why Do People Assign Such a High Weight in Their Financial Plan to It?

Usually, I would tell people that you can split what you spend on into two different groups:

- The more essential spending. Usually inflexible and more important to you.

- The less essential spending. Usually, we can be more flexible about it.

In income planning, you could have different sources of income that differ in what they are made up of and may have different characteristics. You might trust some strategies more than others.

So the question is, do you:

- More essential spending <—– Use the more trusted income strategy.

- Less essential spending <—– Use the less trusted income strategy.

Or do you do the opposite:

- More essential spending <—– Use the less trusted income strategy.

- Less essential spending <—– Use the more trusted income strategy.

I would guess that most of us would select the former, but really, we are selecting an income strategy that matches our unique needs better.

An income strategy that involves CPF is divisive in whether we consider that as a more conservative or a more risky strategy. If you either living off CPF interest or CPF LIFE, both have non-volatile asset value characteristics and therefore appear safer.

But most of us know that there is government policy risk in that these could change on a whim.

The alternative is to craft your own income strategy and usually it is based around:

- Property rental income.

- Dividend income from listed and unlisted stocks and bond securities.

- More popular recently is to create your own income wrapper around ETFs and unit trust.

- A combination of the above.

The downside of any of the plan above is that:

- Markets are uncertain and your asset value will be volatile.

- Depending on each of ours sophistication, our income stream is either going to be volatile or we face the uncertainty that we will run out of money prematurely. (Basically you have sophistication and implementation risk)

We can argue all day whether #1 and #2 is a fact but most people overrate their strategy ability to remain non-volatile and safe. They are just more risky in nature.

But… with a self-crafted income strategy, you don’t have policy risk.

So which strategy is more conservative? I think most would still select the former and that using a income strategy with policy risk to match your most essential spending is preferred.

Sometimes, I am unsure if I am the weird one because I prefer the second.

In fact, I think most who pursue the path of F.I. prefer the second. We sought to find our own investment and income strategy we preferred and trust because for the people in most countries, they:

- Don’t trust the government’s execution fully that the income will be there.

- Prefers the flexibility to extract income from their financial assets earlier than the usual retirement age.

- Have more autonomy.

I felt that the government-based system will have that glaring policy risk weakness which makes it odd to apply that to match the most essential spending.

But many people will choose to match that with their most important stuff.

The weirdest is when I hear someone say that… after they develop financial anxiety due to their past investment experience, they felt safe that they could always rely on their CPF money or CPF LIFE. This gives them confidence to be risky with their cash investments.

If you ask them, they would not dismiss the policy risks as well.

But I think many just threw caution to the wind that most changes will be “within their own mental parameters”.

I find it weird that you can experience safety and security with a strategy like that to use that as the most important part of whatever Kueh Lapis strategy or whatever you call it (In Providend, we call this the Income bucket or income floor).

And now… we see some crying father and mother because of these policy changes.

The bigger problem might be their judgement that such a wealth management strategy is safe and secure.

They should relook how they think about safety, probability and the reliance that they are lucky in their wealth management planning than to cry father and cry mother.

Embrace Volatility in Your Wealth Building

There is unhappiness because, for the majority, they are uncomfortable with the concept of

- Asset value volatility

- Income volatility

- Uncertainty over the success rate of their strategies

So when something that some how doesn’t have these characteristics taken away from them, there is real fear that manifest into anger.

Sometimes, we have to ask whether there is this free lunch out there that we have this golden goose that lays 4% p.a. always with no downside.

Sometimes the greatest risk is not something you can see but the stuff you choose to ignore or are uncomfortable with.

Our uncomfortableness to risk usually made us seek out scam-like investments (not that CPF or government pensions are).

Living with volatility can be challenging but there can be a sweet spot somewhere.

I am very glad that we struggled and learn these things earlier because learning and struggling with risk assets early help us:

- Understand the pros and cons in investments and wealth management strategies through real-life experiences.

- Grow more comfortable living with them.

It is okay to experience uncomfortableness early and lose little, but develop a deeper, intricate awareness than to live in an artificial environment.

You could… but if you are forced into a dangerous environment then would you be able to survive?

There are sweet spots out there in the risk curve to earn more than 4%, if you match your time horizon with the minimum required tenor of some investments out there. The earlier we learn about this the better.

Conclusion

Those with a good financial head thought that most of the CPF moves is for the better. They are more aligned to the core objectives as well.

The positive ones see the silver lining that there is an opportunity for more consistent income in retirement.

I am disappointed sometimes by the thought leadership in the finance space. We should be giving people the right clarity and explain what this means to most or different group of Singaporeans.

But we are left with more fear which manifests into anger.

I do think the wealth management industry will be in glee over this announcement because you need “critical problems” to push out “much-needed sophisticated solutions”.

This is good for our business.

I think I should start polishing up my Allianz Income & Growth slide deck instead of writing so much here.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

The post Mr Lawrence Wong Woke Up on Friday Morning and Chose Violence. appeared first on Investment Moats.